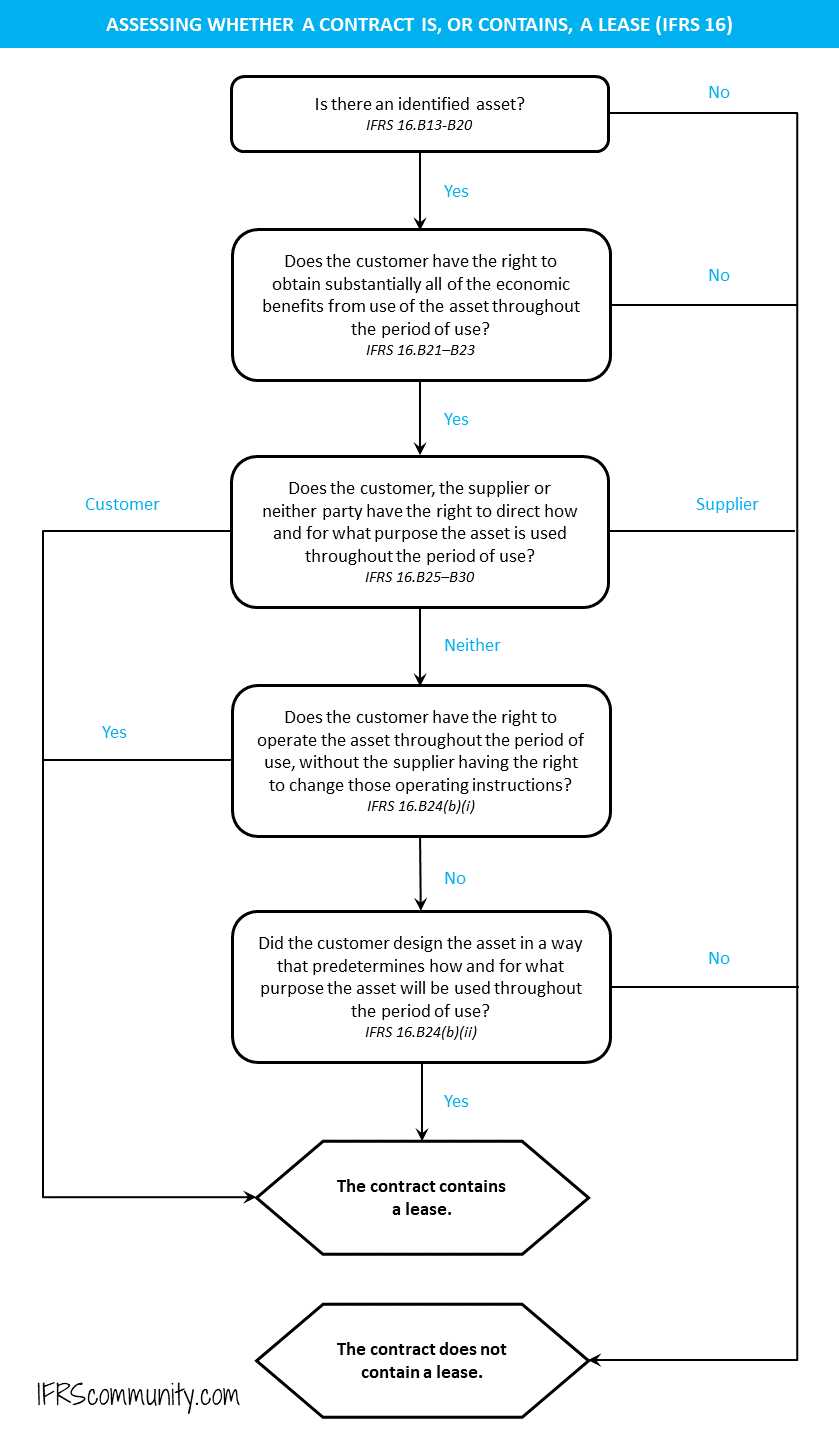

Identifiable Asset: Definition, Applications, Illustration

Definition of Identifiable Asset

An identifiable asset is any asset that can be separately identified and measured. This includes tangible assets such as buildings, machinery, and inventory, as well as intangible assets such as patents, trademarks, and customer relationships. These assets have a specific value that can be determined through various valuation methods.

Applications of Identifiable Assets

Furthermore, identifiable assets are used in collateral for loans and financing. Lenders often require borrowers to provide collateral, which can be in the form of identifiable assets, to secure the loan. This provides lenders with a guarantee that they can recover their investment in case of default.

Illustration of Identifiable Asset

For example, consider a manufacturing company that owns a factory building, machinery, and inventory. These tangible assets can be easily identified and measured. The company also holds patents for its unique manufacturing process and trademarks for its brand name. These intangible assets are also identifiable and have a specific value.

When valuing the company, the identifiable assets are taken into account, and their value is determined through various valuation methods. This helps investors, lenders, and other stakeholders understand the financial health and potential of the company.

Definition of Identifiable Asset

An identifiable asset is a tangible or intangible resource that can be separately identified and reliably measured. It is an asset that has a specific value and can be distinguished from other assets. This means that it can be bought, sold, or transferred independently of other assets.

Identifiable assets can include physical assets such as buildings, machinery, and equipment, as well as intangible assets such as patents, trademarks, and copyrights. These assets are typically recorded on a company’s balance sheet and are used to generate revenue or provide other economic benefits.

For an asset to be considered identifiable, it must meet certain criteria. First, it must be capable of being separated or divided from the entity and sold, transferred, licensed, rented, or exchanged. Second, it must arise from contractual or other legal rights. Finally, it must be capable of producing future economic benefits.

| Examples of Identifiable Assets | Explanation |

|---|---|

| Real Estate | Land, buildings, and other physical properties owned by a company. |

| Patents | Exclusive rights granted to inventors for their inventions. |

| Trademarks | Distinctive signs, logos, or symbols used to identify a company’s products or services. |

| Goodwill | The excess of the purchase price over the fair value of the identifiable net assets acquired in a business combination. |

| Customer Lists | Lists of customers and their contact information, which are valuable assets for businesses. |

Applications of Identifiable Assets

Identifiable assets play a crucial role in various aspects of business operations and financial management. Here are some key applications of identifiable assets:

1. Financial Reporting

Identifiable assets are essential for accurate financial reporting. These assets are recorded on the balance sheet and provide valuable information about a company’s financial position. They help investors, creditors, and other stakeholders assess the company’s ability to generate future cash flows and meet its obligations.

2. Valuation

Identifiable assets are used in the valuation of a company or its individual business units. These assets, such as tangible assets like property, plant, and equipment, or intangible assets like patents and trademarks, contribute to the overall value of the company. Valuation techniques like the market approach, income approach, and cost approach rely on the identification and assessment of these assets.

3. Mergers and Acquisitions

Identifiable assets play a significant role in mergers and acquisitions (M&A) transactions. When companies merge or acquire other businesses, the identification and valuation of the target company’s assets are crucial for determining the purchase price and negotiating the deal. Identifiable assets also help in assessing the synergies and potential risks associated with the transaction.

4. Risk Management

Identifiable assets are important for risk management purposes. By identifying and assessing the value of assets, companies can determine their exposure to various risks, such as market risk, operational risk, and credit risk. This information helps companies develop strategies to mitigate these risks and protect their assets.

5. Capital Budgeting

Identifiable assets are considered when making investment decisions and capital budgeting. Companies evaluate the potential returns and risks associated with investing in new assets or projects. Identifiable assets provide information about the expected cash flows, useful life, and potential risks, which are crucial for determining the feasibility and profitability of the investment.

Illustration of Identifiable Asset

Let’s consider a practical example to illustrate the concept of an identifiable asset. Imagine a company called XYZ Corp. that operates in the technology industry. XYZ Corp. has recently acquired a smaller company, ABC Corp., which specializes in developing software applications.

Step 1: Identification of Assets

After the acquisition, XYZ Corp. needs to identify the assets it has acquired from ABC Corp. This includes tangible assets such as office equipment, furniture, and computers, as well as intangible assets such as patents, copyrights, and software licenses.

Step 2: Valuation of Assets

Once the assets have been identified, XYZ Corp. needs to determine their fair market value. This involves assessing the value of tangible assets based on their current market prices and estimating the value of intangible assets based on their future earning potential.

Step 3: Recording the Assets

After the valuation process, XYZ Corp. records the identifiable assets on its balance sheet. This allows the company to track the value of its assets and provide transparency to its stakeholders.

Step 4: Utilization of Assets

XYZ Corp. can now start utilizing the acquired assets to enhance its operations and generate revenue. For example, the company can use the software applications developed by ABC Corp. to improve its own products or offer them as standalone solutions to customers.

Step 5: Monitoring and Maintenance

It is crucial for XYZ Corp. to monitor and maintain the identifiable assets to ensure their continued value and usefulness. This includes regular maintenance of office equipment, updating software applications, and protecting intellectual property rights.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.