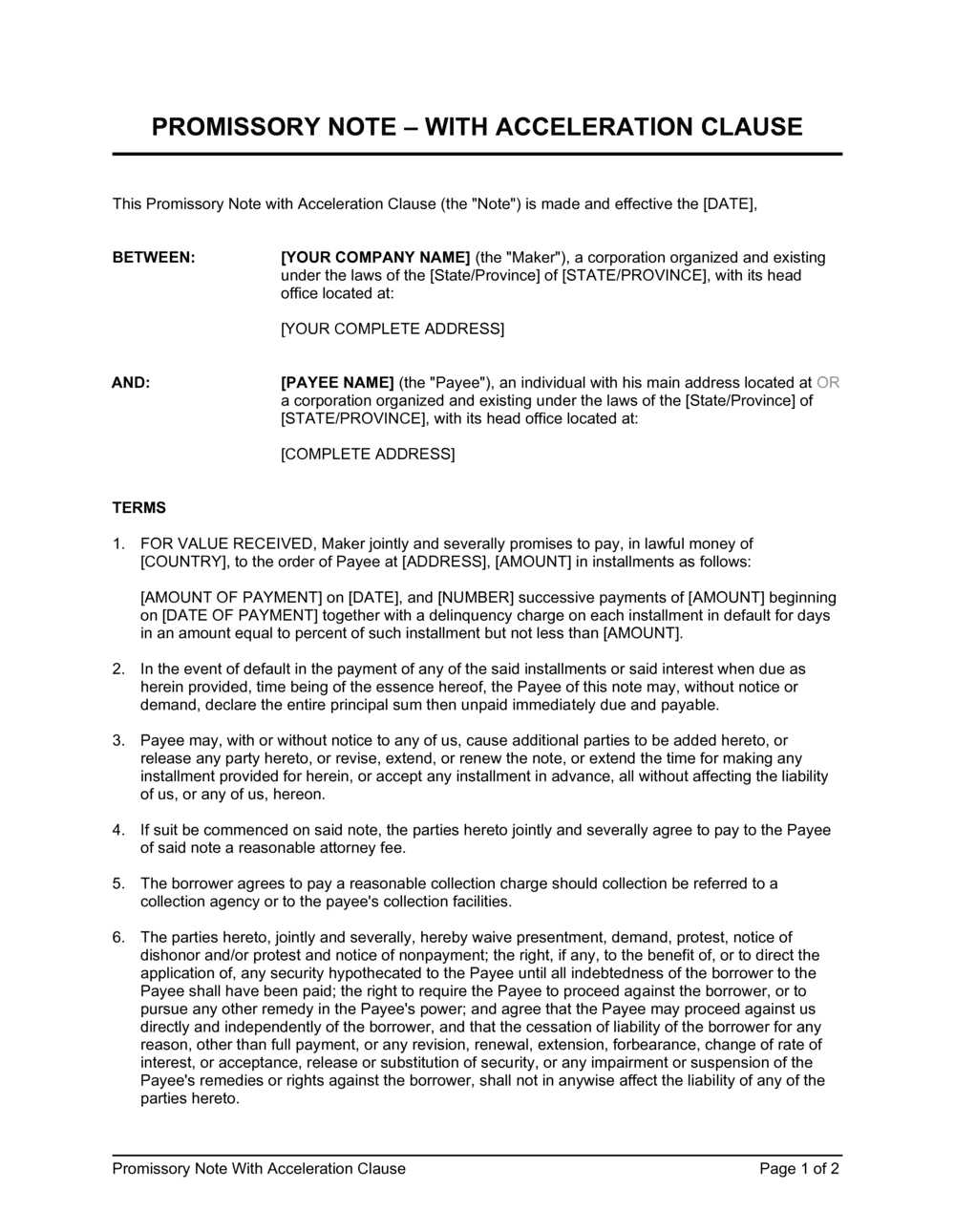

What is an Acceleration Clause?

An acceleration clause is a provision in a loan agreement that allows the lender to demand immediate repayment of the entire outstanding balance if certain conditions are not met by the borrower. It essentially accelerates the repayment schedule of the loan, requiring the borrower to pay off the loan in full rather than making regular installment payments over time.

Acceleration clauses are commonly found in mortgage agreements and other types of loans. They are designed to protect the lender’s interests by providing a remedy in case the borrower defaults on the loan or fails to meet specific obligations outlined in the loan agreement.

Overall, an acceleration clause is a powerful tool for lenders to protect their interests and ensure timely repayment of loans. However, it also places a significant responsibility on borrowers to fulfill their obligations and avoid defaulting on the loan.

Definition and Explanation

An acceleration clause is a provision commonly found in loan agreements that allows the lender to demand immediate repayment of the entire outstanding balance if certain conditions are not met by the borrower. This clause essentially “accelerates” the repayment schedule, requiring the borrower to pay off the loan in full rather than making regular installment payments over time.

Acceleration clauses are typically included in loan agreements to protect the lender’s interests and provide them with a remedy if the borrower fails to meet their obligations. These clauses are often triggered by specific events, such as defaulting on payments, breaching the terms of the loan agreement, or declaring bankruptcy.

How Does an Acceleration Clause Work?

Examples of Acceleration Clauses

Here are a few examples of how acceleration clauses can be worded in loan agreements:

- If the borrower fails to make three consecutive monthly payments, the lender may accelerate the loan and demand immediate repayment of the outstanding balance.

- If the borrower files for bankruptcy, the lender may immediately accelerate the loan and demand full repayment.

Benefits of Including an Acceleration Clause

From the lender’s perspective, including an acceleration clause in a loan agreement provides several benefits. Firstly, it acts as a deterrent, as borrowers are less likely to default on their payments or breach the terms of the agreement knowing that the lender can demand immediate repayment. Secondly, it provides the lender with a quicker and more efficient way to recover their funds in the event of default, rather than having to pursue lengthy legal proceedings.

For borrowers, the presence of an acceleration clause serves as a reminder to fulfill their obligations and make timely payments. It also allows them to better understand the consequences of defaulting on the loan and encourages responsible financial behavior.

Why Lenders Use Acceleration Clauses

Lenders use acceleration clauses as a means of protecting their investments and mitigating risk. By including this provision in loan agreements, lenders can ensure that they have the ability to recover their funds in a timely manner if the borrower fails to meet their obligations. This helps to safeguard their financial interests and minimize potential losses.

Acceleration clauses also provide lenders with leverage in negotiations and can act as a deterrent against potential defaulters. Knowing that the lender can accelerate the loan and demand immediate repayment can motivate borrowers to fulfill their obligations and make timely payments.

Considerations for Borrowers

Borrowers should also consider the potential impact of an acceleration clause on their financial situation. If they are unable to repay the loan in full within the specified timeframe, they may face legal action, foreclosure, or repossession of collateral. It’s crucial to assess one’s ability to meet the repayment requirements before agreeing to a loan with an acceleration clause.

How Does an Acceleration Clause Work?

An acceleration clause is a provision in a loan agreement that allows the lender to demand immediate repayment of the entire loan balance if certain conditions are not met by the borrower. This clause is typically included in mortgage agreements, car loans, and other types of loans where the lender wants to protect their interests.

Conditions for Triggering an Acceleration Clause

The specific conditions for triggering an acceleration clause can vary depending on the loan agreement. However, common triggers include:

- Failure to make timely loan payments

- Defaulting on the loan

- Declaring bankruptcy

- Selling the collateral without the lender’s permission

Consequences of Triggering an Acceleration Clause

If an acceleration clause is triggered, the borrower must repay the loan in full within the specified time frame. If they are unable to do so, the lender may take legal action to recover the outstanding balance. This can result in the borrower’s assets being seized or their wages being garnished.

In addition to the financial consequences, triggering an acceleration clause can also have a negative impact on the borrower’s credit score. This can make it more difficult for them to obtain future loans or credit.

It is important for borrowers to carefully review loan agreements and understand the terms and conditions, including any acceleration clauses, before signing.

Examples of Acceleration Clauses

An acceleration clause is a provision in a loan agreement that allows the lender to demand immediate repayment of the entire outstanding balance if certain conditions are not met. Here are some examples of acceleration clauses:

| Example | Description |

|---|---|

| Missed Payments | If the borrower fails to make consecutive monthly payments, the lender may invoke the acceleration clause and require the borrower to repay the entire loan amount. |

| Violation of Loan Terms | If the borrower violates any terms of the loan agreement, such as using the loan funds for unauthorized purposes, the lender may accelerate the loan and demand immediate repayment. |

| Change in Ownership | If there is a change in ownership of the property used as collateral for the loan, the lender may require the borrower to repay the loan in full. |

| Default on Other Obligations | If the borrower defaults on other obligations, such as failing to pay taxes or other debts, the lender may invoke the acceleration clause and demand immediate repayment. |

These examples illustrate the various circumstances in which an acceleration clause may be triggered. It is important for borrowers to understand the potential consequences of such clauses and to carefully review the terms of their loan agreements before signing.

Benefits of Including an Acceleration Clause

An acceleration clause is a provision in a loan agreement that allows the lender to demand immediate repayment of the entire loan balance if certain conditions are not met by the borrower. While this clause may seem disadvantageous to borrowers, it actually offers several benefits for both parties involved.

1. Protection for Lenders

The inclusion of an acceleration clause provides protection for lenders by ensuring that they have the ability to recover their funds in a timely manner. If a borrower fails to make timely payments or breaches other terms of the loan agreement, the lender can invoke the acceleration clause and demand full repayment. This helps lenders mitigate the risk of default and potential losses.

2. Increased Borrower Accountability

By including an acceleration clause in a loan agreement, borrowers are held accountable for meeting their obligations. The possibility of having to repay the entire loan balance can serve as a strong incentive for borrowers to make timely payments and adhere to the terms of the agreement. This promotes responsible borrowing behavior and reduces the likelihood of default.

3. Flexibility for Borrowers

While an acceleration clause may seem restrictive, it can actually provide flexibility for borrowers in certain situations. For example, if a borrower comes into a significant amount of money or receives a windfall, they have the option to repay the loan in full without incurring any additional interest or penalties. This can help borrowers save money in the long run and potentially improve their financial situation.

4. Negotiating Power

The inclusion of an acceleration clause can give borrowers additional negotiating power when obtaining a loan. Lenders may be more willing to offer favorable terms, such as lower interest rates or longer repayment periods, if they have the security of an acceleration clause in place. This can result in cost savings for borrowers and make the loan more affordable.

Why Lenders Use Acceleration Clauses

An acceleration clause is a provision that is commonly included in loan agreements by lenders. This clause gives the lender the right to demand immediate repayment of the entire loan balance if certain conditions are not met by the borrower. While this may seem like a harsh provision, there are several reasons why lenders use acceleration clauses.

1. Mitigating Risk

One of the main reasons lenders include acceleration clauses in loan agreements is to mitigate their risk. By having the ability to accelerate the loan and demand immediate repayment, lenders can protect themselves in case the borrower defaults on the loan or fails to meet certain obligations. This helps lenders minimize their potential losses and ensures that they can recover their funds as quickly as possible.

2. Encouraging Borrower Compliance

Acceleration clauses can also serve as a deterrent for borrowers who may be considering defaulting on their loan or not fulfilling their obligations. The threat of having to repay the entire loan balance immediately can motivate borrowers to stay current on their payments and meet all the terms of the loan agreement. This ultimately benefits both the lender and the borrower, as it reduces the likelihood of default and helps maintain a positive lending relationship.

3. Providing Flexibility

Acceleration clauses can provide lenders with flexibility in managing their loan portfolios. If a lender needs to free up capital or if market conditions change, they can exercise the acceleration clause to call in the loan and use the funds for other purposes. This can be particularly beneficial in situations where the lender needs to respond quickly to changing economic conditions or investment opportunities.

4. Protecting Collateral

For loans that are secured by collateral, such as real estate or vehicles, acceleration clauses can help protect the lender’s interest in the collateral. If the borrower defaults on the loan, the lender can accelerate the loan and take possession of the collateral to recover their funds. This ensures that the lender has a legal mechanism to enforce their rights and recoup their losses in case of default.

| Benefits of Acceleration Clauses for Lenders |

|---|

| Mitigating risk |

| Encouraging borrower compliance |

| Providing flexibility |

| Protecting collateral |

Considerations for Borrowers

While acceleration clauses are primarily designed to protect lenders, borrowers should also carefully consider the implications of these clauses before entering into a loan agreement. Here are a few key considerations for borrowers:

1. Financial Stability

Before signing a loan agreement with an acceleration clause, borrowers should assess their financial stability and ability to make timely payments. If there is a risk of defaulting on the loan, triggering the acceleration clause could result in the entire loan balance becoming due immediately.

2. Prepayment Penalties

Borrowers should also review the loan agreement to determine if there are any prepayment penalties associated with the acceleration clause. These penalties could make it more expensive for borrowers to pay off the loan early or refinance the loan.

3. Negotiation

It may be possible for borrowers to negotiate the terms of the acceleration clause with the lender before signing the loan agreement. This could include setting a longer notice period or establishing specific conditions that must be met before the acceleration clause can be triggered.

4. Legal Advice

Before entering into a loan agreement with an acceleration clause, borrowers should consider seeking legal advice to fully understand the implications and potential risks. A lawyer can review the terms of the agreement and provide guidance on how to protect the borrower’s interests.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.