What is Equilibrium Quantity?

Equilibrium quantity is a concept in economics that refers to the quantity of a good or service that is demanded and supplied in a market at a specific price level. It represents the point at which the quantity demanded by consumers is equal to the quantity supplied by producers.

Definition and Explanation

In a market, the equilibrium quantity is determined by the interaction of demand and supply. Demand refers to the quantity of a good or service that consumers are willing and able to buy at a given price, while supply refers to the quantity that producers are willing and able to sell at a given price.

At any price level, there is a corresponding quantity demanded and quantity supplied. When the quantity demanded exceeds the quantity supplied, there is a shortage in the market, leading to upward pressure on prices. Conversely, when the quantity supplied exceeds the quantity demanded, there is a surplus in the market, leading to downward pressure on prices.

The equilibrium quantity occurs when the quantity demanded is equal to the quantity supplied. At this point, there is no shortage or surplus in the market, and the price remains stable. It represents a state of balance between the desires of consumers and the capabilities of producers.

Factors Affecting Equilibrium Quantity

Several factors can affect the equilibrium quantity in a market. These include changes in consumer preferences, changes in the prices of related goods, changes in income levels, changes in production costs, and government policies or regulations.

For example, if consumer preferences shift towards a particular good, the demand for that good may increase, leading to an increase in the equilibrium quantity. On the other hand, if production costs rise, producers may be less willing to supply the good, leading to a decrease in the equilibrium quantity.

Relationship between Equilibrium Quantity and Price

When the quantity demanded and supplied are not equal, market forces push the price towards the equilibrium level. If the quantity demanded exceeds the quantity supplied, prices will rise until the market reaches equilibrium. If the quantity supplied exceeds the quantity demanded, prices will fall until the market reaches equilibrium.

Definition and Explanation

Equilibrium quantity refers to the quantity of a good or service that is bought and sold in a market when the supply and demand for that good or service are in balance. It represents the point at which the quantity demanded by consumers is equal to the quantity supplied by producers.

In a competitive market, the equilibrium quantity is determined by the interaction of supply and demand. When the price of a good or service is too high, the quantity demanded by consumers will be lower than the quantity supplied by producers, resulting in a surplus. On the other hand, when the price is too low, the quantity demanded will be higher than the quantity supplied, leading to a shortage.

The equilibrium quantity is the quantity at which there is neither a surplus nor a shortage in the market. At this point, the price is stable, and there is no pressure for it to change. Producers are able to sell all of their goods or services, and consumers are able to purchase the quantity they desire.

Determinants of Equilibrium Quantity

Several factors can affect the equilibrium quantity in a market. These include:

1. Changes in consumer preferences: If consumer preferences shift towards a particular good or service, the equilibrium quantity may increase as demand increases.

2. Changes in production costs: If the cost of producing a good or service increases, producers may supply less of it, resulting in a decrease in the equilibrium quantity.

3. Changes in technology: Technological advancements can increase the efficiency of production, leading to an increase in the equilibrium quantity.

4. Changes in government regulations: Government policies and regulations can impact the equilibrium quantity by imposing restrictions or incentives on production or consumption.

Furthermore, policymakers can use the concept of equilibrium quantity to design effective regulations and policies that promote market efficiency and stability. By considering the factors that affect the equilibrium quantity, policymakers can make informed decisions that benefit both producers and consumers.

Factors Affecting Equilibrium Quantity

In economics, equilibrium quantity refers to the quantity of a good or service that is produced and consumed in a market when supply and demand are in balance. It is the point at which the quantity demanded by consumers equals the quantity supplied by producers. Several factors can affect the equilibrium quantity in a market, including:

1. Price

2. Production Costs

The production costs of a good or service also play a crucial role in determining the equilibrium quantity. If the production costs increase, producers may be less willing or able to supply the same quantity at a given price. This can lead to a decrease in the equilibrium quantity. On the other hand, if production costs decrease, producers may be able to supply more at the same price, resulting in an increase in the equilibrium quantity.

3. Technological Advances

Technological advances can have a significant impact on the equilibrium quantity. Improved technology can lead to increased production efficiency, allowing producers to supply more goods or services at the same cost. This can result in an increase in the equilibrium quantity. Conversely, if technology becomes outdated or less efficient, it can lead to a decrease in the equilibrium quantity.

4. Consumer Preferences

Consumer preferences and tastes can also influence the equilibrium quantity. If consumer preferences shift towards a particular product, the demand for that product may increase, leading to an increase in the equilibrium quantity. Conversely, if consumer preferences shift away from a product, the demand may decrease, resulting in a decrease in the equilibrium quantity.

These are just a few of the factors that can affect the equilibrium quantity in a market. It is important for economists and market participants to understand these factors and their impact on supply and demand in order to make informed decisions and predict market outcomes.

Relationship between Equilibrium Quantity and Price

In economics, the concept of equilibrium quantity refers to the quantity of a particular good or service that is bought and sold in a market when supply and demand are in balance. It is the point at which the quantity demanded by consumers is equal to the quantity supplied by producers.

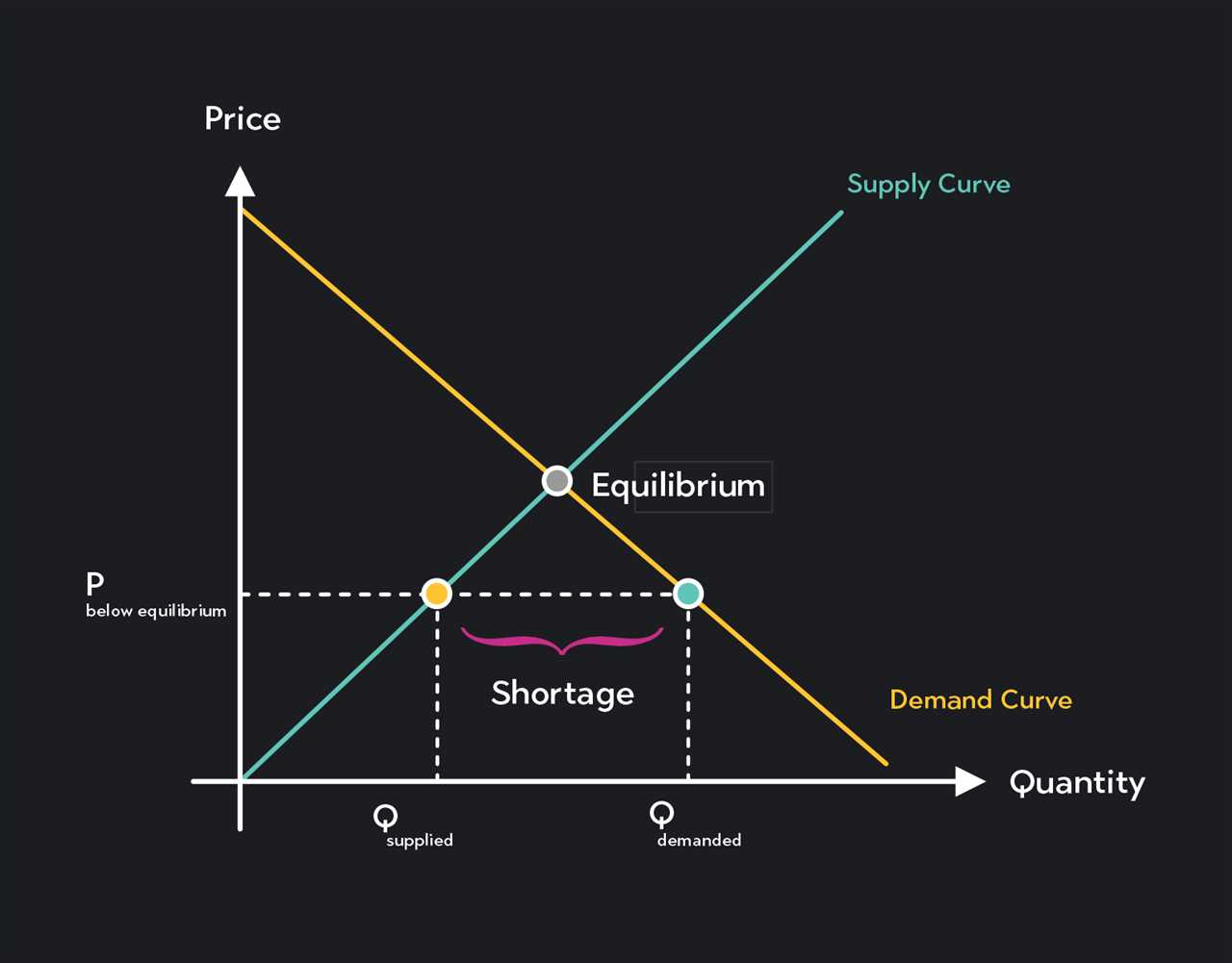

The relationship between equilibrium quantity and price is a fundamental concept in economics. When the price of a good or service is too high, the quantity demanded by consumers decreases, while the quantity supplied by producers increases. This creates a surplus, as producers are unable to sell all of their goods at the higher price.

On the other hand, when the price of a good or service is too low, the quantity demanded by consumers increases, while the quantity supplied by producers decreases. This creates a shortage, as consumers are unable to purchase all of the goods they desire at the lower price.

Therefore, in order to reach equilibrium, the price of a good or service must be set at a level where the quantity demanded by consumers is equal to the quantity supplied by producers. This is the point at which the market clears, and there is neither a surplus nor a shortage of the good or service.

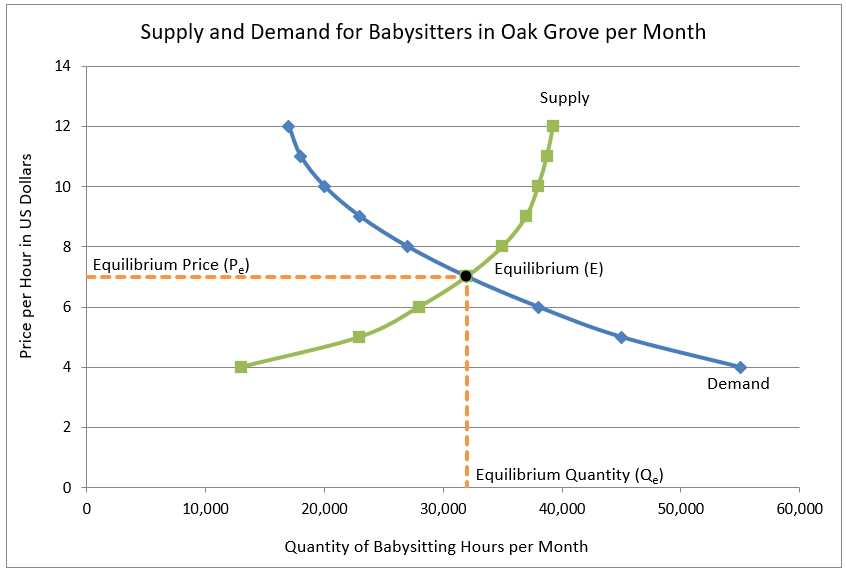

The relationship between equilibrium quantity and price can be represented graphically on a supply and demand diagram. The point at which the supply and demand curves intersect is the equilibrium price, and the corresponding quantity is the equilibrium quantity.

It is important to understand the relationship between equilibrium quantity and price because it helps to determine the efficiency and effectiveness of a market. When a market is in equilibrium, it means that resources are being allocated efficiently and that there is a balance between supply and demand. This leads to a more stable and sustainable market.

However, if the price is set too high or too low, it can lead to market distortions and inefficiencies. For example, if the price is set too high, it may discourage consumers from purchasing the good or service, leading to a decrease in demand. On the other hand, if the price is set too low, it may encourage excessive consumption and lead to a shortage of the good or service.

- Forecasting: Equilibrium quantity provides a basis for forecasting future market trends. By analyzing the factors affecting equilibrium quantity, economists can make predictions about future demand and supply conditions. This information is valuable for businesses in planning their production levels, inventory management, and overall business strategies.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.