Demand for Labor: Definition, Factors, and Role in Economy

The demand for labor is a fundamental concept in economics that refers to the quantity of labor that employers are willing and able to hire at a given wage rate in a specific market or industry. It plays a crucial role in determining the overall employment levels and wage rates in an economy.

There are several factors that influence the demand for labor:

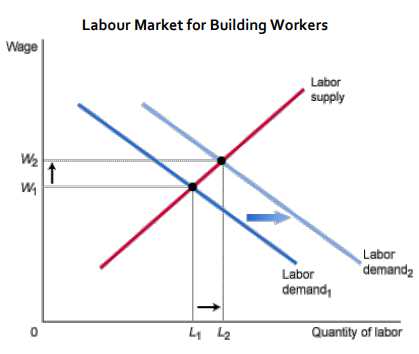

2. Technological Advancements: Technological advancements can significantly affect the demand for labor. The introduction of new technologies often leads to increased productivity, which can reduce the need for labor in certain industries. On the other hand, technological advancements can also create new job opportunities in industries that develop and implement these technologies.

3. Cost of Labor: The cost of labor, including wages, benefits, and other labor-related expenses, is an essential factor in determining the demand for labor. When labor costs increase, firms may reduce their demand for labor by either hiring fewer workers or substituting labor with capital-intensive production methods.

4. Business Cycle: The overall state of the economy, as measured by factors such as GDP growth, consumer spending, and business investment, can influence the demand for labor. During periods of economic expansion, firms tend to experience increased demand for their products or services, leading to higher demand for labor. Conversely, during economic downturns, firms may reduce their workforce to cut costs.

5. Government Policies: Government policies, such as labor regulations, minimum wage laws, and tax incentives, can have a significant impact on the demand for labor. For example, an increase in the minimum wage may lead to a decrease in the demand for low-skilled workers, as firms may find it more cost-effective to substitute labor with automation or outsource certain tasks.

The concept of demand for labor refers to the quantity of labor that employers are willing and able to hire at a given wage rate in a specific market or industry. It is a fundamental concept in economics and plays a crucial role in determining the equilibrium wage rate and employment level in a labor market.

The demand for labor is derived from the demand for the goods and services produced by the labor. As businesses produce more goods and services, they require more labor to meet the increased demand. Conversely, if the demand for goods and services decreases, businesses may reduce their labor force to adjust to the lower demand.

Several factors influence the demand for labor. One of the primary factors is the overall level of economic activity. When the economy is growing, businesses tend to expand their operations and hire more workers. Conversely, during a recession or economic downturn, businesses may reduce their workforce to cut costs.

Technological advancements also play a significant role in shaping the demand for labor. As technology improves, businesses may automate certain tasks, reducing the need for human labor. This can lead to a decrease in the demand for certain types of jobs while increasing the demand for workers with skills in operating and maintaining technology.

The composition of the workforce and the skills of the labor force also impact the demand for labor. If there is a shortage of workers with specific skills or qualifications, businesses may struggle to find suitable candidates, leading to an increase in the demand for those workers. On the other hand, if there is an oversupply of workers with certain skills, the demand for those workers may decrease.

Government policies and regulations can also influence the demand for labor. For example, minimum wage laws can increase the cost of labor for businesses, potentially leading to a decrease in the demand for low-skilled workers. Similarly, labor market regulations, such as restrictions on hiring and firing, can affect the flexibility of businesses to adjust their workforce.

Factors Influencing the Demand for Labor

The demand for labor is influenced by various factors that play a crucial role in determining the quantity of labor that employers are willing and able to hire. These factors can be broadly categorized into two main groups: external and internal factors.

External Factors

External factors refer to the conditions and circumstances outside of the specific organization or industry that affect the demand for labor. These factors include:

1. Economic conditions: The overall state of the economy, including factors such as GDP growth, inflation, and interest rates, can significantly impact the demand for labor. During periods of economic expansion, businesses tend to experience increased demand for their products or services, leading to a higher demand for labor. Conversely, during economic downturns, businesses may reduce their workforce to cut costs.

2. Technological advancements: The rapid pace of technological advancements has a profound impact on the demand for labor. Automation and artificial intelligence have the potential to replace certain job functions, leading to a decrease in the demand for labor in those areas. On the other hand, technological advancements can also create new job opportunities, increasing the demand for labor in emerging industries.

3. Government regulations: Government policies and regulations, such as minimum wage laws, labor market regulations, and tax policies, can influence the demand for labor. For example, an increase in the minimum wage may lead to higher labor costs for businesses, potentially reducing their demand for labor.

Internal Factors

Internal factors refer to the characteristics and decisions specific to an organization or industry that affect the demand for labor. These factors include:

1. Business strategy and objectives: The strategic goals and objectives of a business can influence its demand for labor. For example, a company that aims to expand its market share may require additional labor to support its growth plans.

2. Productivity and efficiency: The level of productivity and efficiency within an organization can impact the demand for labor. Businesses that are able to achieve higher levels of productivity may require fewer workers to produce the same output, leading to a lower demand for labor.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.