Generally Accepted Accounting Principles (GAAP)

Generally Accepted Accounting Principles (GAAP) are a set of standards and guidelines that govern the accounting practices and financial reporting of companies. These principles ensure that financial statements are prepared in a consistent and transparent manner, allowing investors and stakeholders to make informed decisions.

Definition of GAAP

GAAP is a framework of accounting principles, standards, and procedures that are widely accepted and followed by companies in the United States. It provides a common language for financial reporting and ensures that financial statements are comparable across different companies and industries.

Standards of GAAP

GAAP consists of a set of standards issued by the Financial Accounting Standards Board (FASB), a private, non-profit organization. These standards cover various aspects of financial reporting, including revenue recognition, expense recognition, asset valuation, and disclosure requirements. By following these standards, companies can ensure that their financial statements are accurate, reliable, and useful to users.

Rules of GAAP

Overall, GAAP plays a crucial role in maintaining the integrity and transparency of financial reporting. It helps investors, creditors, and other stakeholders to assess the financial health and performance of companies, make informed decisions, and compare financial information across different entities. Compliance with GAAP is essential for companies seeking to gain the trust and confidence of investors and stakeholders.

Definition of GAAP

Generally Accepted Accounting Principles (GAAP) refer to a set of accounting standards and guidelines that are widely recognized and followed by companies when preparing their financial statements. These principles provide a framework for consistent and reliable financial reporting, ensuring that financial information is presented in a clear and understandable manner.

GAAP is essential for the smooth functioning of the financial markets as it enhances transparency and comparability of financial statements. It allows investors, creditors, and other stakeholders to make informed decisions based on accurate and reliable financial information.

GAAP encompasses a broad range of principles and rules that cover various aspects of accounting, including revenue recognition, expense recognition, asset valuation, and disclosure requirements. These principles are based on the accrual basis of accounting, which recognizes revenues and expenses when they are earned or incurred, regardless of when cash is received or paid.

One of the key features of GAAP is its principle-based approach. This means that while GAAP provides general guidelines, it allows for flexibility and judgment in applying these principles to specific situations. Companies are required to exercise professional judgment and make informed estimates when applying GAAP to ensure that the financial statements fairly represent their financial position and performance.

It is important to note that GAAP is not a static set of rules. It evolves over time to keep up with changes in the business environment and accounting practices. The Financial Accounting Standards Board (FASB) is the primary body responsible for establishing and updating GAAP in the United States.

In summary, GAAP is a set of accounting principles and guidelines that provide a framework for consistent and reliable financial reporting. It plays a crucial role in ensuring transparency and comparability of financial statements, allowing stakeholders to make informed decisions. GAAP is based on the accrual basis of accounting and allows for flexibility in its application to specific situations.

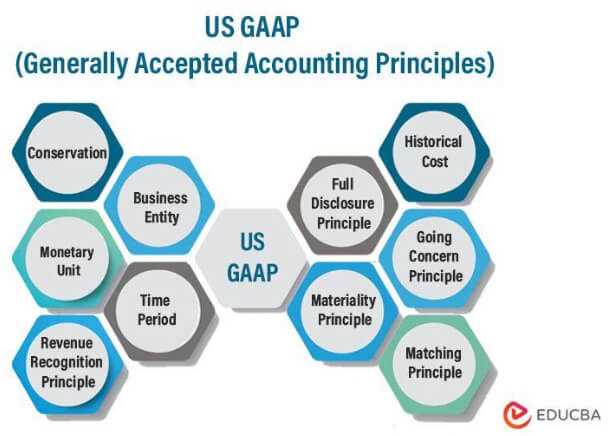

Standards of GAAP

Generally Accepted Accounting Principles (GAAP) are a set of standards and guidelines that dictate how financial statements should be prepared and presented. These standards ensure consistency and comparability in financial reporting, allowing investors, creditors, and other stakeholders to make informed decisions.

1. FASB

The Financial Accounting Standards Board (FASB) is the primary body responsible for establishing and updating GAAP in the United States. It sets the standards through a transparent and inclusive process that involves input from various stakeholders, including accountants, auditors, investors, and regulators.

2. Principles-based approach

GAAP follows a principles-based approach, which means that it provides broad guidelines rather than specific rules. This approach allows for flexibility and judgment in applying the standards to different situations. It recognizes that every business is unique and that a one-size-fits-all approach may not be appropriate.

3. Materiality

Materiality is a key concept in GAAP. It requires companies to disclose information that could influence the decisions of users of financial statements. Materiality is determined based on the nature and magnitude of an item, as well as its potential impact on the financial statements as a whole.

4. Consistency

Consistency is another important principle of GAAP. It requires companies to apply the same accounting methods and principles consistently from one period to another. This allows for meaningful comparisons of financial information over time and enhances the reliability and usefulness of financial statements.

5. Full disclosure

Full disclosure is a fundamental principle of GAAP. It requires companies to provide all relevant and material information in their financial statements and accompanying notes. This includes information about significant accounting policies, contingencies, related party transactions, and other relevant matters.

6. Going concern

The going concern assumption is a fundamental concept in GAAP. It assumes that a company will continue to operate in the foreseeable future. This assumption allows for the recognition of assets, liabilities, revenues, and expenses based on their expected future economic benefits or obligations.

By adhering to these standards, companies can provide transparent and reliable financial information that helps stakeholders assess their financial performance and make informed decisions. Compliance with GAAP is essential for maintaining the integrity of financial reporting and promoting trust in the financial markets.

Rules of GAAP

Generally Accepted Accounting Principles (GAAP) are a set of standards and guidelines that govern the preparation and presentation of financial statements. These rules ensure consistency and comparability in financial reporting, allowing investors, creditors, and other stakeholders to make informed decisions.

There are several key rules that form the foundation of GAAP:

1. Historical Cost Principle

The historical cost principle states that assets should be recorded at their original cost when acquired. This means that the value of an asset is based on the amount paid to acquire it, rather than its current market value. This principle provides a reliable and objective basis for measuring and reporting assets.

2. Revenue Recognition Principle

The revenue recognition principle determines when and how revenue should be recognized in financial statements. According to this principle, revenue should be recognized when it is earned and realized or realizable. This means that revenue should be recorded when goods are delivered or services are rendered, and when payment is reasonably assured.

3. Matching Principle

4. Full Disclosure Principle

The full disclosure principle requires that all relevant and material information should be disclosed in the financial statements and accompanying notes. This principle ensures that users of the financial statements have access to all necessary information to make informed decisions.

5. Consistency Principle

The consistency principle states that once an accounting method or principle has been chosen, it should be consistently applied from one period to another. This principle ensures that financial statements are comparable over time, allowing users to analyze trends and make meaningful comparisons.

CORPORATE FINANCE BASICS

One important concept in corporate finance is the Generally Accepted Accounting Principles (GAAP). GAAP refers to a set of standards and rules that govern the preparation and reporting of financial statements. These principles ensure consistency and transparency in financial reporting, allowing investors, creditors, and other stakeholders to make informed decisions.

The definition of GAAP encompasses a wide range of principles and guidelines that are followed by companies when preparing their financial statements. These principles cover areas such as revenue recognition, expense recognition, asset valuation, and financial statement presentation.

The standards of GAAP provide specific guidance on how to apply the principles in different situations. For example, the Financial Accounting Standards Board (FASB) in the United States sets the standards for GAAP. These standards are regularly updated to reflect changes in the business environment and accounting practices.

The rules of GAAP outline the specific requirements that companies must follow when preparing their financial statements. These rules ensure that companies provide accurate and reliable information to users of financial statements. Examples of GAAP rules include the requirement to use accrual accounting, the need to disclose significant accounting policies, and the use of specific formats for financial statements.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.