The Definition and Implications of Capitalizing Costs

But what does this mean and what are the implications for businesses?

Capitalizing costs allows businesses to spread the cost of certain assets over their useful life, rather than recognizing the full cost as an expense in the period the asset is acquired. This can have several benefits for businesses, including:

| 1. Improved accuracy of financial statements: | By capitalizing costs, businesses can more accurately reflect the value of their assets on the balance sheet. This can provide a clearer picture of the company’s financial health and performance. |

| 2. Smoother income recognition: | Capitalizing costs allows businesses to avoid large fluctuations in their income statement due to the immediate recognition of expenses. Instead, the costs are spread out over time, resulting in a more consistent and stable income recognition. |

| 3. Increased asset value: | By capitalizing costs, businesses can increase the value of their assets on the balance sheet. This can improve the company’s financial ratios and make it more attractive to investors and lenders. |

| 4. Tax benefits: | Capitalizing costs can also provide tax benefits for businesses. By spreading out the cost of assets over their useful life, businesses can potentially reduce their taxable income and lower their tax liability. |

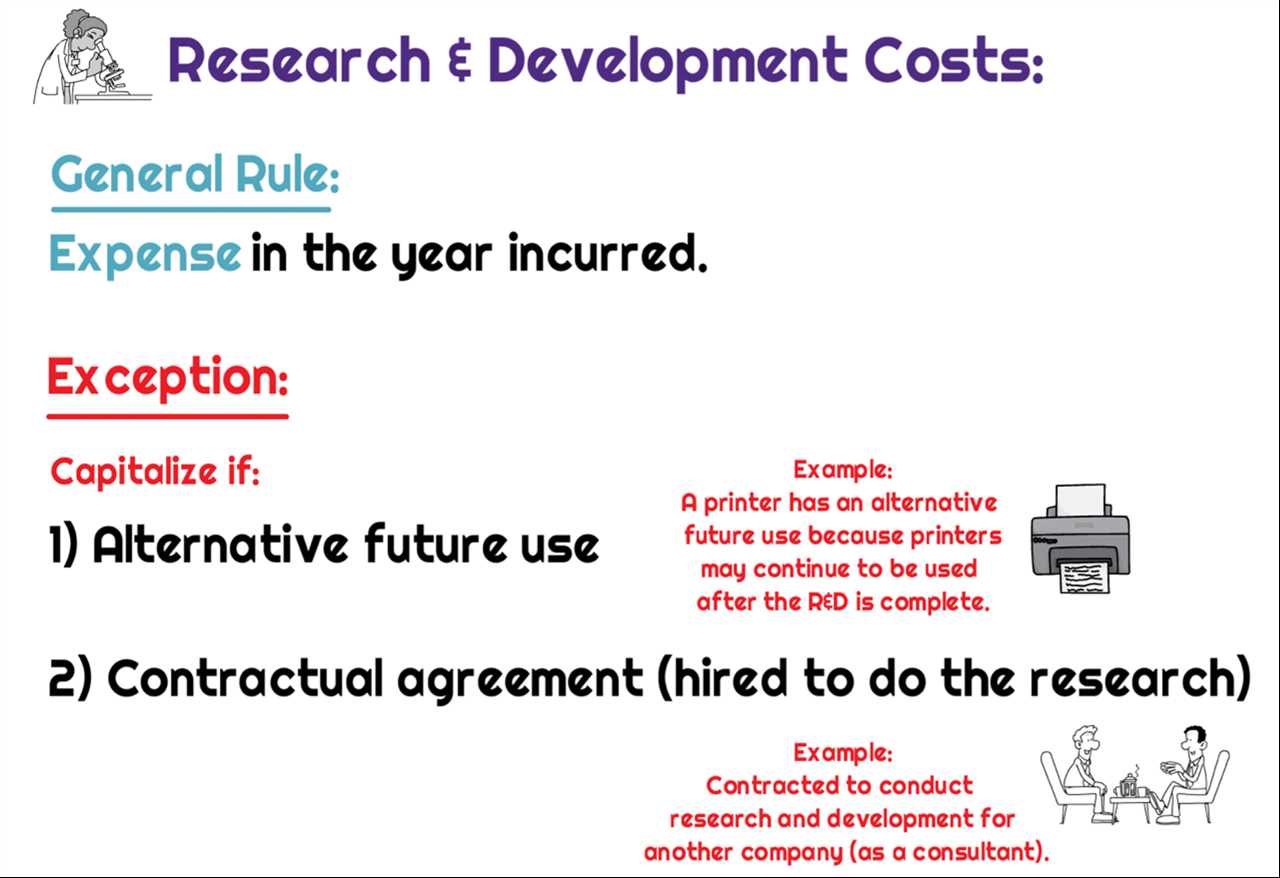

However, it is important for businesses to understand that not all costs can be capitalized. Generally, costs that can be capitalized include the purchase price of assets, direct costs of acquisition, and costs incurred to bring the asset to its intended use. On the other hand, costs that are considered routine repairs and maintenance, or costs that do not add value to the asset, should be expensed immediately.

The Definition and Implications of Capitalizing Costs

But what does this mean exactly? When a cost is capitalized, it is treated as an investment in the company’s future benefits, rather than a current expense. This has important implications for how the cost is reported and accounted for.

By capitalizing costs, a company is essentially spreading out the recognition of the expense over time, rather than taking the full hit in the period in which the cost is incurred. This can have the effect of smoothing out the company’s reported earnings and improving its financial ratios.

On the other hand, costs that cannot be capitalized are typically those that are considered to be ordinary and necessary expenses of running a business. These costs are immediately recognized as expenses on the income statement and are deducted from revenue to determine net income.

Financial Statements

Financial statements are essential documents that provide a snapshot of a company’s financial health. They are used by investors, creditors, and other stakeholders to assess the company’s performance and make informed decisions.

Importance of Financial Statements

Financial statements provide valuable information about a company’s profitability, liquidity, and solvency. They include the balance sheet, income statement, cash flow statement, and statement of changes in equity.

The balance sheet shows the company’s assets, liabilities, and shareholders’ equity at a specific point in time. It provides a snapshot of the company’s financial position and helps assess its solvency.

The cash flow statement shows the company’s cash inflows and outflows over a specific period. It helps assess the company’s liquidity and ability to generate cash.

The statement of changes in equity shows the changes in the company’s shareholders’ equity over a specific period. It helps assess the company’s financial health and the impact of various transactions on shareholders’ equity.

Interpreting Financial Statements

Some key financial ratios include the current ratio, which measures the company’s liquidity; the debt-to-equity ratio, which measures its leverage; and the return on equity, which measures its profitability.

By analyzing financial statements, investors can assess the company’s financial health, growth potential, and risk profile. Creditors can evaluate the company’s ability to repay its debts, while other stakeholders can make informed decisions about their involvement with the company.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.