What is the De Minimis Tax Rule?

The De Minimis Tax Rule is a regulation that applies to municipal bonds, which are issued by state and local governments to finance public projects such as infrastructure improvements, schools, and hospitals. The rule determines whether the interest earned from these bonds is subject to federal income tax.

Definition and Explanation

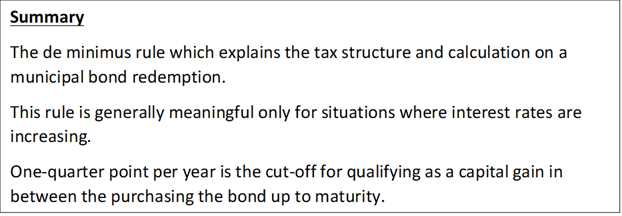

The De Minimis Tax Rule states that if the total amount of tax-exempt interest earned from municipal bonds in a tax year is less than a certain threshold, it is considered de minimis and is not subject to federal income tax. This threshold is set by the Internal Revenue Service (IRS) and is adjusted annually for inflation.

The purpose of the De Minimis Tax Rule is to provide a small tax benefit to individual investors who earn a minimal amount of tax-exempt interest. It recognizes that the administrative burden of reporting and taxing these small amounts of interest may outweigh the potential revenue gained by the government.

Calculation of De Minimis Tax Rule

To calculate whether the interest earned from municipal bonds falls under the de minimis threshold, you need to add up the tax-exempt interest from all municipal bonds you own. If the total amount is below the threshold, you do not need to report or pay federal income tax on that interest.

The de minimis threshold for the current tax year can be found in the IRS guidelines or obtained from a tax professional. It is important to note that this threshold may vary depending on your filing status and other factors, so it is advisable to consult the most up-to-date information.

Example of De Minimis Tax Rule

Let’s say you own municipal bonds from different issuers and the tax-exempt interest earned from each bond is as follows:

- Bond A: $500

- Bond B: $300

- Bond C: $200

To determine if the total interest earned falls under the de minimis threshold, you would add up the amounts:

$500 + $300 + $200 = $1,000

It is important to keep accurate records of your municipal bond investments and consult a tax professional to ensure compliance with the De Minimis Tax Rule and other tax regulations.

Definition and Explanation

The De Minimis Tax Rule is a provision in the tax code that allows taxpayers to exclude small amounts of income from their taxable income. This rule is designed to provide relief for taxpayers who have minimal income or receive small amounts of income that would be impractical to report.

Under the De Minimis Tax Rule, taxpayers are allowed to exclude income that is below a certain threshold from their taxable income. This threshold is determined by the IRS and may vary from year to year. The purpose of this rule is to simplify the tax reporting process for taxpayers and reduce the administrative burden on both taxpayers and the IRS.

The De Minimis Tax Rule is often applied to income from sources such as interest, dividends, and capital gains. For example, if an individual earns $10 in interest income from a savings account, they may be able to exclude this income from their taxable income under the De Minimis Tax Rule.

It is important to note that the De Minimis Tax Rule applies only to certain types of income and has specific limitations. Taxpayers should consult with a tax professional or refer to the IRS guidelines to determine if they qualify for the De Minimis Tax Rule and how to properly report their income.

Calculation of De Minimis Tax Rule

The calculation of the De Minimis Tax Rule is a method used to determine whether the interest income from certain municipal bonds is subject to federal income tax. This rule applies to individuals and corporations who hold these bonds.

To calculate the De Minimis Tax Rule, you need to know the bond’s face value, the bond’s yield, and the bond’s maturity date. The face value is the amount that the bond will pay at maturity, and the yield is the annual interest rate that the bond will pay. The maturity date is the date when the bond will expire.

The formula for calculating the De Minimis Tax Rule is as follows:

For example, let’s say you have a municipal bond with a face value of $10,000, an annual interest rate of 4%, and a maturity date of December 31, 2025. Today’s date is January 1, 2022.

First, calculate the bond’s annual interest by multiplying the face value by the annual interest rate:

Bond’s Annual Interest = $10,000 x 0.04 = $400

Next, calculate the number of days remaining until the bond’s maturity date:

Finally, calculate the De Minimis Tax Rule by dividing the bond’s annual interest by the bond’s face value and multiplying by the number of days remaining:

De Minimis Tax Rule = ($400 / $10,000) x 1,096 = $43.84

It is important to note that the De Minimis Tax Rule may vary depending on the individual’s or corporation’s tax situation and the specific regulations in their jurisdiction. Consulting with a tax professional is recommended to ensure accurate calculation and compliance with tax laws.

Formula and Method

The calculation of the De Minimis Tax Rule involves a specific formula and method. The formula is as follows:

De Minimis Tax Rule = (Annual Interest Income / Adjusted Gross Income) x 100

The method for applying the De Minimis Tax Rule is straightforward. If the calculated De Minimis Tax Rule percentage is below a certain threshold, typically 2%, the taxpayer is exempt from paying taxes on the interest income earned from municipal bonds. However, if the percentage exceeds the threshold, the taxpayer is required to report and pay taxes on the interest income.

It is important to note that the specific threshold percentage may vary depending on the tax laws and regulations of a particular jurisdiction. Taxpayers should consult with their tax advisors or refer to the applicable tax code to determine the exact threshold percentage for their situation.

By utilizing the formula and method of the De Minimis Tax Rule, taxpayers can determine whether they are eligible for tax exemption on their municipal bond interest income. This rule provides a mechanism to encourage investment in municipal bonds by offering tax benefits to individuals with relatively low interest income compared to their overall income.

Example of De Minimis Tax Rule

Let’s consider an example to understand how the De Minimis Tax Rule works. Suppose you are an investor who purchased municipal bonds with a face value of $100,000. The bonds have a coupon rate of 4% and pay interest semi-annually. The bonds mature in 10 years.

According to the De Minimis Tax Rule, if the total amount of interest received from the municipal bonds throughout the year is less than $10, the investor is not required to report it as taxable income.

Interest payment = Face value of the bond * Coupon rate / 2

Interest payment = $100,000 * 4% / 2 = $2,000

Since the interest payment is $2,000, which is greater than $10, the investor is required to report it as taxable income.

However, if the interest payment was less than $10, for example, $5, the investor would not be required to report it as taxable income. This is because it falls below the De Minimis threshold.

It is important to note that the De Minimis Tax Rule applies to each individual bond. If an investor holds multiple municipal bonds, the interest payments from each bond should be considered separately to determine if they meet the De Minimis threshold.

Illustration and Case Study

To better understand the application of the De Minimis Tax Rule, let’s consider a case study involving municipal bonds. Municipal bonds are debt securities issued by state and local governments to finance public projects such as infrastructure development, schools, and hospitals.

Suppose an investor purchases $100,000 worth of municipal bonds with a coupon rate of 4%. This means that the investor will receive $4,000 in interest income annually. However, not all of this income is subject to federal income tax.

Now, let’s calculate the taxable portion of the interest income using the De Minimis Tax Rule formula:

Therefore, the investor will have to pay federal income tax on $3,800 of the interest income generated from the municipal bonds.

The De Minimis Tax Rule is designed to simplify the tax reporting process for small amounts of income. By exempting de minimis income from taxation, taxpayers can avoid the administrative burden of reporting and paying taxes on minimal amounts of interest income.

Municipal Bonds and De Minimis Tax Rule

Municipal bonds are a type of debt security issued by state and local governments to finance public projects such as infrastructure improvements, schools, and hospitals. These bonds are attractive to investors because the interest income they generate is typically exempt from federal income tax and, in some cases, state and local taxes as well.

Definition and Explanation

The De Minimis Tax Rule is designed to prevent wealthy individuals from taking advantage of the tax-exempt status of municipal bond interest by investing a large amount of money in a single bond issue. If an individual receives more than a de minimis amount of tax-exempt interest from a particular bond issue, a portion of that interest may be subject to federal income tax.

The de minimis amount is determined based on a formula that takes into account the total amount of tax-exempt interest received by the individual and the total amount of tax-exempt interest issued by the bond. The formula is complex and may vary depending on the specific circumstances of the investor and the bond issue.

Calculation of De Minimis Tax Rule

The calculation of the de minimis amount involves comparing the individual’s tax-exempt interest from a particular bond issue to the total tax-exempt interest issued by the bond. If the individual’s tax-exempt interest exceeds a certain percentage of the total tax-exempt interest, a portion of that interest may be subject to federal income tax.

For example, if an individual holds $1 million worth of a bond issue that generates $100,000 in tax-exempt interest, and the total tax-exempt interest issued by the bond is $1 million, the de minimis amount would be 10% ($100,000 / $1 million). If the individual’s tax-exempt interest exceeds 10% of the total tax-exempt interest, a portion of that interest may be subject to federal income tax.

Example of De Minimis Tax Rule

Illustration and Case Study

If John’s tax-exempt interest exceeds 25% of the total tax-exempt interest, a portion of that interest may be subject to federal income tax. For example, if John’s tax-exempt interest is $600,000, which is 30% of the total tax-exempt interest, $100,000 of that interest may be subject to federal income tax.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.