What is Microeconomics?

Microeconomics is a branch of economics that focuses on the behavior of individuals and firms in making decisions regarding the allocation of limited resources. It is concerned with the study of how households and businesses make choices and how these choices affect the market outcomes.

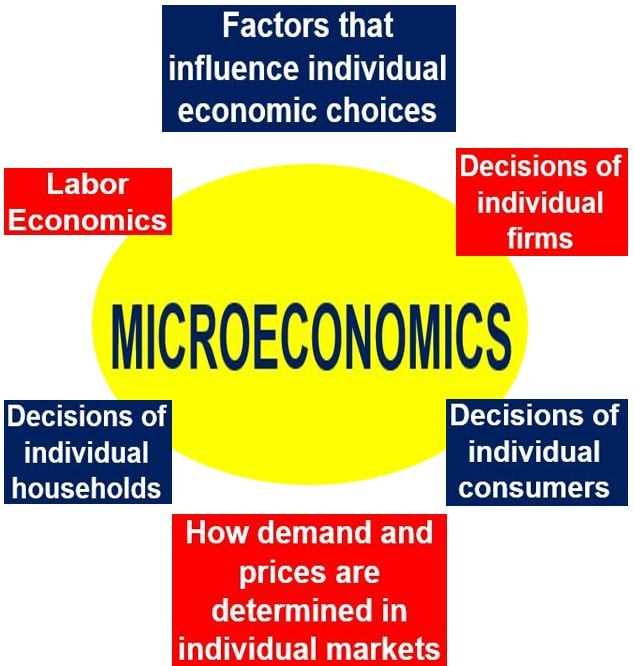

Scope of Microeconomics

The scope of microeconomics is vast and covers various aspects of economic analysis. It examines the behavior of individual consumers and producers, the determination of prices and quantities in specific markets, and the interaction between different market participants.

Microeconomics analyzes the principles of supply and demand, which are the fundamental forces that determine prices in the market. It studies how changes in prices and incomes affect consumer behavior and the choices they make. It also looks at the factors that influence the production decisions of firms, such as costs, technology, and market competition.

Key Concepts in Microeconomics

- Scarcity: Microeconomics recognizes that resources are limited and must be allocated efficiently to meet unlimited wants and needs.

- Opportunity Cost: This concept refers to the cost of choosing one option over another. When making decisions, individuals and firms must consider the value of the next best alternative that is given up.

- Supply and Demand: The interaction between supply and demand determines the equilibrium price and quantity in a market. Supply represents the quantity of a good or service that producers are willing to offer, while demand represents the quantity that consumers are willing to buy.

- Elasticity: Elasticity measures the responsiveness of quantity demanded or supplied to changes in price or income. It helps determine how sensitive consumers and producers are to price changes.

- Market Structures: Microeconomics examines different market structures, such as perfect competition, monopoly, oligopoly, and monopolistic competition. Each structure has unique characteristics that affect market outcomes and the behavior of firms.

Applications of Microeconomics

1. Consumer Behavior

2. Producer Behavior

3. Market Analysis

Microeconomics plays a crucial role in analyzing markets. It examines the forces of supply and demand to determine equilibrium prices and quantities in different markets. Microeconomists study market structures, such as perfect competition, monopoly, oligopoly, and monopolistic competition, to understand the behavior of firms and the efficiency of market outcomes.

4. Public Policy

Microeconomics provides insights into the design and evaluation of public policies. It helps policymakers understand the impact of various interventions, such as taxes, subsidies, price controls, and regulations, on market outcomes and social welfare. Microeconomists analyze the trade-offs involved in policy decisions and provide recommendations for improving economic efficiency and equity.

5. International Trade

Key Concepts in Microeconomics

Supply and Demand

One of the key concepts in microeconomics is supply and demand. Supply refers to the quantity of a good or service that producers are willing and able to sell at a given price. Demand, on the other hand, refers to the quantity of a good or service that consumers are willing and able to buy at a given price. The interaction of supply and demand determines the equilibrium price and quantity in a market.

Elasticity

Elasticity is another important concept in microeconomics. It measures the responsiveness of quantity demanded or quantity supplied to changes in price or income. Price elasticity of demand measures how sensitive the quantity demanded is to changes in price, while price elasticity of supply measures how sensitive the quantity supplied is to changes in price.

Income elasticity of demand measures how sensitive the quantity demanded is to changes in income. Elasticity helps economists understand how changes in price or income affect consumer behavior and producer decisions.

Opportunity Cost

Opportunity cost is the concept that refers to the value of the next best alternative foregone when making a decision. It is a fundamental concept in microeconomics as it helps individuals and firms make rational choices. By considering the opportunity cost, individuals and firms can weigh the benefits and costs of different options and make informed decisions.

For example, if a person decides to spend money on a vacation, the opportunity cost would be the value of the next best alternative, such as investing the money or saving it for future use.

Market Structures

Microeconomics also examines different market structures, which refer to the characteristics of a market that influence the behavior of firms and the outcomes in the market. The four main market structures are perfect competition, monopoly, oligopoly, and monopolistic competition.

In perfect competition, there are many buyers and sellers, and no single firm has control over the market price. Monopoly, on the other hand, occurs when there is only one seller in the market. Oligopoly is a market structure with a few large firms dominating the market, while monopolistic competition is characterized by many firms selling differentiated products.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.