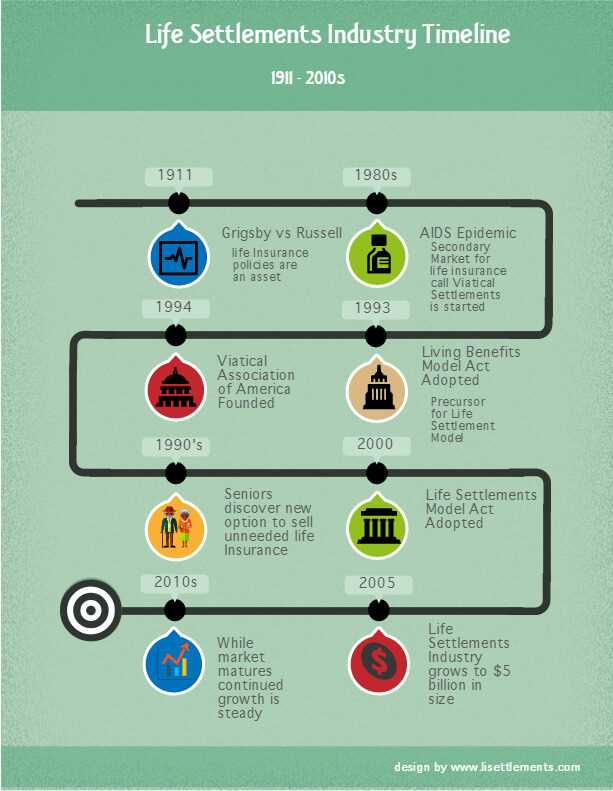

What is a Life Settlement?

A life settlement is a financial transaction in which a policyholder sells their life insurance policy to a third party in exchange for a lump sum payment. This is typically done when the policyholder no longer needs or can afford the policy, or when they would prefer to receive a cash payout rather than continuing to pay premiums.

Definition and Explanation

A life settlement is often referred to as a “secondary market for life insurance” because it allows policyholders to sell their policies to investors who are willing to pay more than the surrender value offered by the insurance company. The investor then becomes the new owner of the policy and assumes responsibility for paying future premiums and collecting the death benefit when the insured passes away.

Life settlements are regulated by state laws and require a licensed life settlement provider to facilitate the transaction. The provider acts as an intermediary between the policyholder and the investor, ensuring that the transaction is fair and compliant with all applicable regulations.

Benefits of Life Settlements

There are several benefits to pursuing a life settlement:

- Financial Flexibility: Life settlements provide policyholders with a lump sum payment that can be used for any purpose, such as paying off debt, funding retirement, or covering medical expenses.

- Higher Payout: Selling a life insurance policy through a life settlement often results in a higher payout than surrendering the policy to the insurance company.

- Relief from Premium Payments: By selling their policy, policyholders are relieved of the ongoing premium payments, which can be a significant financial burden.

- Opportunity for Investors: Life settlements offer investors the opportunity to purchase life insurance policies at a discount and potentially earn a return on their investment when the insured passes away.

Overall, life settlements provide a valuable option for policyholders who no longer need or can afford their life insurance policies, allowing them to access the financial benefits of their policy while they are still alive.

Definition and Explanation

A life settlement is a financial transaction in which a policyholder sells their life insurance policy to a third party for a lump sum payment. The buyer of the policy becomes the new owner and beneficiary of the policy, assuming all future premium payments and receiving the death benefit when the insured passes away.

The concept of life settlements emerged as a result of the growing need for policyholders to access the value of their life insurance policies while they are still alive. Many individuals find themselves in situations where their life insurance policies are no longer needed or affordable, and selling the policy provides them with a way to receive a cash payout that can be used for various purposes.

Life settlements are typically available to individuals who are aged 65 or older, although some policies may allow younger individuals to participate. The value of the life settlement is determined by several factors, including the policy’s death benefit, the insured’s age and health status, and the future premium payments required to keep the policy in force.

How Does a Life Settlement Work?

When a policyholder decides to pursue a life settlement, they typically work with a licensed life settlement provider or broker who helps facilitate the transaction. The provider evaluates the policy and determines its market value based on the aforementioned factors.

If the policyholder accepts the offer, the buyer will assume ownership of the policy and become responsible for all future premium payments. The policyholder receives a lump sum payment, which is typically a percentage of the policy’s face value but can vary depending on the specific terms of the transaction.

After the transaction is complete, the buyer will continue to pay the policy’s premiums and will receive the death benefit when the insured passes away. The policyholder no longer has any financial obligations or rights to the policy.

Benefits of Life Settlements

Life settlements offer several benefits to policyholders who are looking to sell their life insurance policies. Some of the key benefits include:

| 1. Financial Flexibility: | By selling their life insurance policy, policyholders can access a significant amount of cash that can be used for various purposes, such as paying off debts, funding retirement, or covering medical expenses. |

| 2. Higher Payout: | In many cases, the lump sum payment received from a life settlement is higher than the surrender value offered by the insurance company. This allows policyholders to maximize the value of their policy. |

| 3. No More Premium Payments: | Once the policy is sold, the policyholder is relieved of the obligation to make future premium payments. This can provide significant financial relief, especially for individuals who are struggling to afford the premiums. |

| 4. Opportunity to Convert an Unneeded Asset: | For policyholders who no longer need or want their life insurance policy, a life settlement provides an opportunity to convert it into a valuable asset that can be used to meet their current financial needs. |

Overall, life settlements offer a viable solution for policyholders who are looking to unlock the value of their life insurance policies. By selling their policies, individuals can gain financial flexibility, access higher payouts, eliminate premium payments, and convert an unneeded asset into cash.

Benefits of Life Settlements

Life settlements offer several benefits for policyholders who are looking to sell their life insurance policies. Here are some of the key advantages:

- Financial Gain: One of the primary benefits of a life settlement is the potential for a significant financial gain. By selling their life insurance policy, policyholders can receive a lump sum payment that is often higher than the surrender value offered by the insurance company.

- Flexibility: Life settlements provide policyholders with greater flexibility in managing their financial assets. The lump sum payment received from a life settlement can be used to pay off debts, cover medical expenses, invest in other opportunities, or simply improve the policyholder’s quality of life.

- No More Premium Payments: When a policyholder sells their life insurance policy through a life settlement, they are relieved of the burden of paying future premium payments. This can be especially beneficial for individuals who are struggling to afford the premiums or no longer need the coverage.

- Maximizing Policy Value: In some cases, a life settlement can provide policyholders with a higher value for their policy than surrendering it back to the insurance company. This can be particularly advantageous for individuals who have experienced changes in their health or financial circumstances since purchasing the policy.

- Opportunity for Legacy Planning: By selling their life insurance policy through a life settlement, policyholders can have the opportunity to allocate funds towards their legacy planning. This can include gifting the proceeds to loved ones, making charitable donations, or creating a trust for future generations.

- Regain Control: Life settlements allow policyholders to regain control over their life insurance policy. Instead of being locked into a policy that may no longer align with their needs or financial goals, policyholders have the ability to sell the policy and make decisions that better suit their current circumstances.

Overall, life settlements offer a valuable financial option for policyholders who are looking to unlock the value of their life insurance policies. By considering a life settlement, individuals can take advantage of the numerous benefits and opportunities that come with selling their policy.

Advantages and Opportunities

Life settlements offer several advantages and opportunities for policyholders looking to sell their life insurance policies. Here are some key benefits:

1. Financial Flexibility:

A life settlement provides policyholders with the opportunity to access a significant amount of money that would otherwise be tied up in their life insurance policy. This can be especially beneficial for individuals who are facing financial difficulties or need funds for medical expenses or retirement.

2. Higher Payouts:

When selling a life insurance policy through a life settlement, policyholders often receive a higher payout compared to surrendering the policy to the insurance company. This is because life settlement providers are willing to pay a lump sum that is greater than the policy’s cash surrender value.

3. No Premium Payments:

Once a life insurance policy is sold through a life settlement, the policyholder is relieved of any further premium payments. This can be a significant relief for individuals who are struggling to keep up with the financial obligations of maintaining their policy.

4. Opportunity for Investment:

The proceeds from a life settlement can be used as an investment opportunity. Policyholders can choose to invest the lump sum in other financial instruments or assets that may provide higher returns or meet their specific financial goals.

5. Peace of Mind:

By selling their life insurance policy through a life settlement, policyholders can gain peace of mind knowing that they have maximized the value of their policy and have access to funds that can improve their financial situation. This can provide a sense of security and relief.

Overall, life settlements offer policyholders a unique opportunity to unlock the value of their life insurance policies and improve their financial well-being. It is important for individuals considering a life settlement to carefully evaluate their options and consult with professionals to ensure they make an informed decision.

Life Settlement FAQs

Here are some frequently asked questions about life settlements:

1. What is a life settlement?

A life settlement is a financial transaction in which a policyholder sells their life insurance policy to a third party for a lump sum cash payment. The third party becomes the new owner of the policy and is responsible for paying the premiums until the insured person passes away, at which point they receive the death benefit.

2. Who can sell their life insurance policy?

Any individual who is at least 65 years old and has a life insurance policy with a face value of at least $100,000 may be eligible to sell their policy.

3. Why would someone consider a life settlement?

There are several reasons why someone might consider a life settlement:

- They no longer need the life insurance coverage

- They are unable to afford the premiums

- They want to use the funds for other financial needs, such as paying off debt or funding retirement

4. How is the value of a life insurance policy determined?

5. Are life settlements taxable?

In most cases, the proceeds from a life settlement are taxable as ordinary income. However, there may be certain exceptions or exemptions depending on the individual’s circumstances and the specific laws in their jurisdiction. It is recommended to consult with a tax professional for personalized advice.

6. How long does the life settlement process take?

These are just a few of the frequently asked questions about life settlements. If you have any additional questions or would like more information, it is advisable to consult with a qualified financial advisor or life settlement provider.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.