Definition of Underwriting Fees

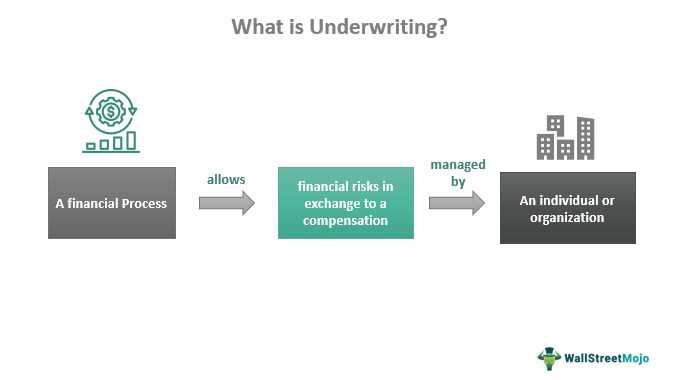

Underwriting fees are charges that insurance companies impose on policyholders to cover the costs associated with the underwriting process. Underwriting is the evaluation and assessment of risks associated with insuring an individual or a business entity.

Underwriting fees are separate from the premium amount and are charged to cover the administrative costs incurred during the underwriting process. These costs include conducting background checks, verifying information provided by the applicant, and processing the necessary paperwork.

It is important to note that underwriting fees are non-refundable, regardless of whether the applicant is approved for insurance coverage or not. These fees are typically paid upfront when applying for a policy and are separate from any other fees or charges associated with the insurance contract.

Underwriting fees vary depending on the insurance company and the type of policy being underwritten. They can range from a fixed amount to a percentage of the premium. It is essential for policyholders to carefully review the terms and conditions of their insurance contract to understand the specific underwriting fees applicable to their policy.

Overall, underwriting fees play a crucial role in covering the costs associated with the evaluation and assessment of risks in the insurance industry. They help insurance companies maintain their operations and ensure the financial stability of the industry as a whole.

Illustrations of Underwriting Fees

Underwriting fees in insurance can vary depending on the type of policy and the specific insurance company. Here are a few illustrations of how underwriting fees may be applied:

Example 1: Auto Insurance

Let’s say you are purchasing auto insurance for your new car. The insurance company will assess the risk associated with insuring your vehicle, such as your driving history, the make and model of your car, and your location. Based on this assessment, they will determine the underwriting fee.

For example, if you have a clean driving record and your car is equipped with advanced safety features, the underwriting fee may be lower. On the other hand, if you have a history of accidents or your car is considered high-risk, the underwriting fee may be higher.

Example 2: Home Insurance

For instance, if you live in an area prone to natural disasters like hurricanes or earthquakes, the underwriting fee may be higher to account for the increased risk. Similarly, if your home is older and requires more maintenance, the underwriting fee may also be higher.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.