Regulation O: Purpose, Applications, and Requirements in Banking

The purpose of Regulation O is to prevent conflicts of interest and ensure fair lending practices within the banking industry. It aims to maintain the integrity of the banking system by imposing restrictions on loans made to insiders, as well as requiring disclosure of these transactions.

Regulation O applies to all banks that are members of the Federal Reserve System, including national banks, state member banks, and bank holding companies. It also applies to nonmember banks that are subsidiaries of bank holding companies.

Under Regulation O, banks are required to obtain prior approval from their board of directors for any loans made to insiders. The approval process involves disclosing the nature of the transaction, the amount of the loan, and any collateral provided. The board of directors must ensure that the loan is made on market terms and is not preferential treatment to the insider.

Furthermore, Regulation O sets limits on the amount of credit that can be extended to insiders. These limits are based on the bank’s capital and surplus, and they aim to prevent excessive lending to insiders that could jeopardize the bank’s financial stability.

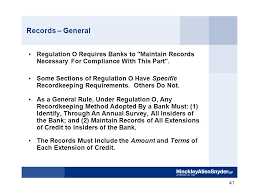

In addition to the approval and credit limits, Regulation O requires banks to maintain records of all insider transactions and submit reports to the Federal Reserve Board on a regular basis. These reports help the regulatory authorities monitor compliance with the regulation and detect any potential violations.

In summary, Regulation O plays a crucial role in ensuring transparency and fairness in lending practices between banks and their insiders. By imposing restrictions, obtaining approval, and setting credit limits, the regulation aims to prevent conflicts of interest and maintain the integrity of the banking system.

Overview of Regulation O

The purpose of Regulation O is to prevent conflicts of interest and ensure fair lending practices within the banking industry. By regulating loans to insiders, the Federal Reserve aims to protect the interests of the bank’s shareholders and depositors.

Under Regulation O, banks are required to establish policies and procedures to prevent preferential treatment or undue risk exposure when granting loans to insiders. These policies should include limits on the amount of credit extended to insiders, as well as guidelines for evaluating the creditworthiness of the borrowers.

One of the key requirements of Regulation O is the reporting of insider loans. Banks are required to report all loans made to insiders, including the terms of the loans and any collateral provided. This reporting helps to ensure transparency and accountability in lending practices.

Violation of Regulation O can result in severe penalties for both the bank and the individuals involved. Banks may face fines, restrictions on lending activities, or even loss of their banking charter. Insiders who knowingly violate the regulation may face personal liability and legal consequences.

Purpose of Regulation O

Preventing Conflicts of Interest

One of the main purposes of Regulation O is to prevent conflicts of interest that may arise when banks lend money to their own insiders. Insiders, such as executive officers and directors, may have significant influence over the decision-making process within the bank. By limiting the loans that can be made to insiders, Regulation O helps to ensure that lending decisions are based on objective criteria and not influenced by personal relationships or self-interest.

By preventing conflicts of interest, Regulation O helps to maintain the integrity and stability of the banking system. It helps to ensure that loans are made based on the creditworthiness of the borrower and the soundness of the loan proposal, rather than personal connections or favors.

Fair Lending Practices

Another important purpose of Regulation O is to promote fair lending practices within financial institutions. By limiting loans to insiders, Regulation O helps to ensure that lending opportunities are available to all customers on an equal basis. It prevents insiders from receiving preferential treatment or access to credit that is not available to the general public.

Regulation O also requires banks to establish and maintain written policies and procedures for making loans to insiders. These policies and procedures must be designed to ensure that loans are made on terms that are consistent with safe and sound banking practices. By establishing these policies and procedures, Regulation O helps to promote transparency and accountability in the lending process.

Applications of Regulation O in Banking

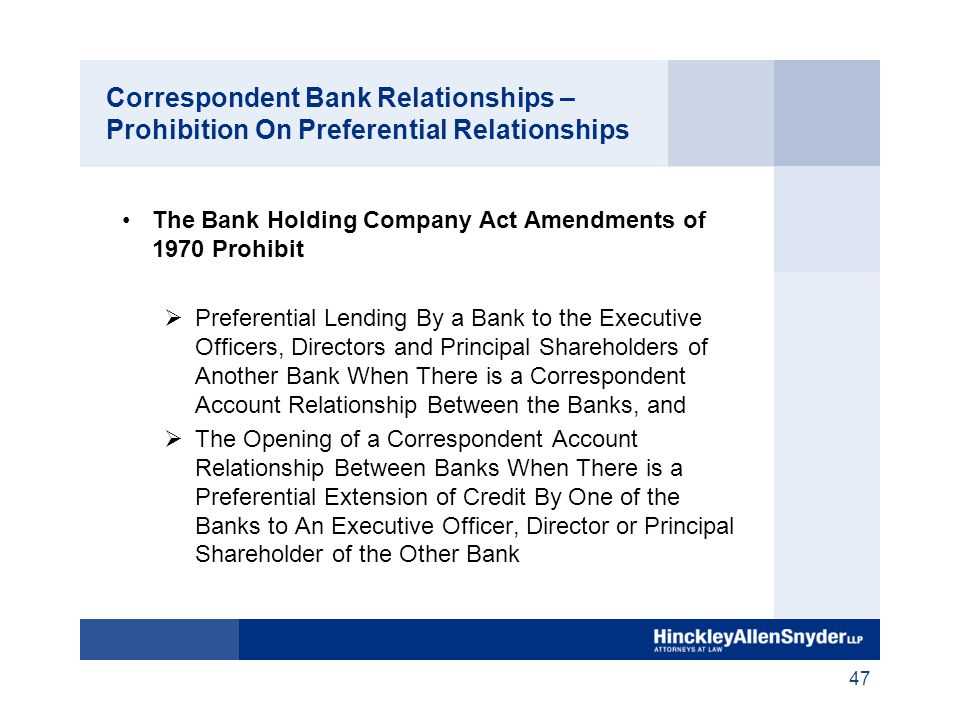

Another application of Regulation O is to regulate loans made by banks to companies controlled by insiders. This helps to prevent self-dealing and conflicts of interest. Banks are required to establish lending limits for these types of loans as well, based on the bank’s capital and surplus.

Regulation O also requires banks to report certain transactions with insiders to their board of directors. This helps to ensure transparency and accountability in the lending process. Banks must report any loans made to insiders, as well as any extensions or renewals of these loans.

Overall, the applications of Regulation O in banking are aimed at promoting fairness, transparency, and accountability in lending practices. By regulating loans to insiders and companies controlled by insiders, Regulation O helps to prevent conflicts of interest and protect the financial stability of banks.

| Applications of Regulation O |

|---|

| Regulating loans to executive officers, directors, and principal shareholders |

| Regulating loans to companies controlled by insiders |

| Establishing lending limits based on capital and surplus |

| Requiring reporting of transactions with insiders |

| Prohibiting preferential lending terms for insiders |

Requirements of Regulation O

Under Regulation O, banks are required to obtain prior approval from their board of directors before extending credit to executive officers, directors, and principal shareholders. This approval must be documented and maintained by the bank.

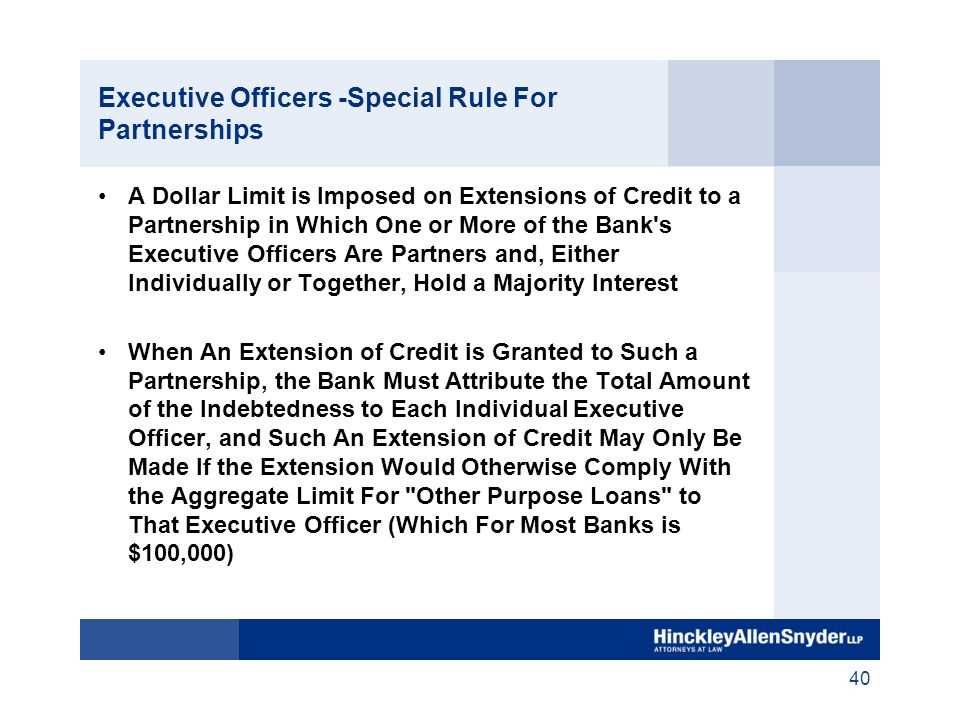

The regulation also sets limits on the amount of credit that can be extended to these individuals. The limits are based on the bank’s capital and surplus, and they vary depending on the type of credit and the relationship between the bank and the borrower.

Banks are also required to establish and maintain a system of recordkeeping to ensure compliance with Regulation O. This includes maintaining records of all extensions of credit covered by the regulation, as well as any approvals obtained from the board of directors.

In addition, banks must disclose certain information regarding their loans to executive officers, directors, and principal shareholders in their annual reports. This information includes the amount of credit outstanding to these individuals, the terms and conditions of the loans, and any changes in the loans during the reporting period.

Noncompliance with Regulation O can result in penalties and enforcement actions by regulatory agencies. These penalties can include fines, restrictions on the bank’s activities, and even removal of the bank’s officers and directors.

Overall, the requirements of Regulation O are designed to promote transparency, accountability, and fairness in banking by preventing insider abuse and conflicts of interest. By imposing these requirements, the regulation helps to maintain the integrity of the banking system and protect the interests of shareholders and depositors.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.