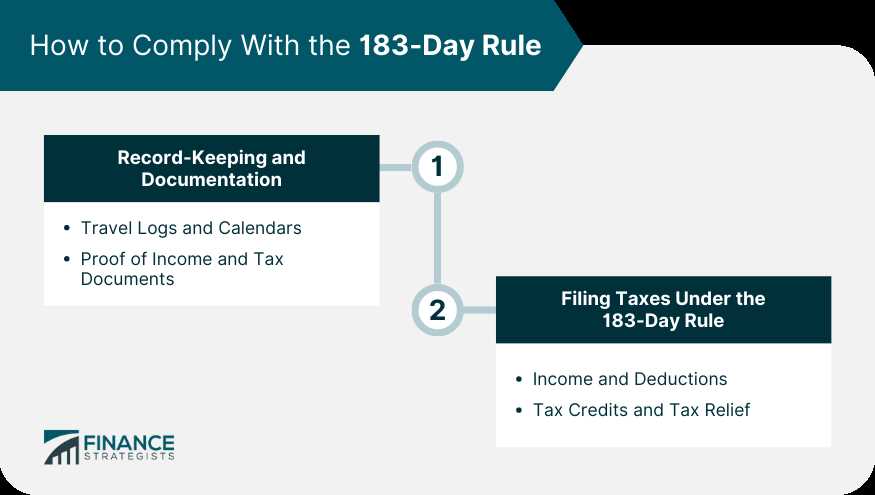

183-Day Rule: Definition and Importance

The 183-day rule is a legal provision used in tax laws to determine an individual’s residency status for tax purposes. It states that if an individual spends 183 days or more in a particular country within a given tax year, they may be considered a resident of that country for tax purposes.

The importance of the 183-day rule lies in its ability to determine an individual’s tax obligations and benefits in a specific country. Being considered a resident for tax purposes can have significant implications on an individual’s tax liability, eligibility for certain tax deductions, and access to various tax benefits and incentives.

For example, if an individual meets the 183-day rule in a particular country, they may be subject to that country’s tax laws and required to report their worldwide income for taxation. On the other hand, if they do not meet the 183-day rule, they may be considered a non-resident and only be required to report income earned within that country.

Additionally, the 183-day rule can also impact an individual’s eligibility for certain tax deductions and benefits. Some countries may offer tax deductions or credits for residents, such as deductions for mortgage interest or education expenses. Meeting the 183-day rule can make an individual eligible for these deductions, while failing to meet it may result in the loss of such benefits.

What is the 183-Day Rule?

The 183-Day Rule is a tax law that determines an individual’s residency status based on the number of days they spend in a particular country. It is used by many countries around the world to determine if a person should be considered a resident for tax purposes.

According to the 183-Day Rule, if an individual spends 183 days or more in a country within a given tax year, they are typically considered a tax resident of that country. This means that they may be subject to paying taxes on their worldwide income in that country.

How does the 183-Day Rule work?

The 183-Day Rule works by counting the number of days an individual spends in a country within a given tax year. This includes both consecutive and non-consecutive days. If the total number of days exceeds the threshold set by the country, the individual is considered a tax resident.

Why is the 183-Day Rule important?

The 183-Day Rule is important because it determines an individual’s tax residency status, which can have significant implications for their tax obligations. Being considered a tax resident of a particular country means that an individual may be required to pay taxes on their worldwide income in that country.

Additionally, the 183-Day Rule can also be used to determine eligibility for certain tax benefits and exemptions. Some countries may offer tax incentives or exemptions to individuals who meet the residency requirements, such as lower tax rates or deductions.

How is the 183-Day Rule Used for Residency?

The 183-Day Rule is a crucial factor in determining an individual’s residency status for tax purposes. It is used by tax authorities to determine whether a person should be considered a resident or non-resident for tax purposes in a particular country.

Under the 183-Day Rule, if an individual spends 183 days or more in a country within a given tax year, they are generally considered a resident for tax purposes in that country. This means that they will be subject to the country’s tax laws and may be required to pay taxes on their worldwide income.

For example, let’s say John is a U.S. citizen who works for a multinational company. He is assigned to work in Germany for a period of one year. If John spends 183 days or more in Germany during that tax year, he will be considered a resident for tax purposes in Germany. As a result, he will be subject to German tax laws and may need to file a tax return in Germany.

It is worth noting that each country may have its own specific rules and criteria for determining residency status. Therefore, it is important for individuals to consult with a tax professional or refer to the tax laws of the specific country to understand how the 183-Day Rule is applied in that jurisdiction.

-Day Rule: Example and Application

The -Day Rule is an important concept in determining an individual’s tax residency status. It is used by tax authorities to determine whether an individual is considered a resident or non-resident for tax purposes. The rule states that if an individual spends 183 days or more in a country within a specific time period, usually a calendar year, they may be considered a tax resident of that country.

Let’s take an example to understand the application of the -Day Rule. Suppose John is a citizen of Country A but has been working in Country B for the past year. John wants to know if he qualifies as a tax resident of Country B based on the -Day Rule.

Based on the -Day Rule, John would be considered a tax resident of Country B for that year. This means that he would be subject to the tax laws and regulations of Country B, including the obligation to file a tax return and pay taxes on his income earned in Country B.

| Related Articles |

|---|

| TAX LAWS |

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.