Federal Housing Administration (FHA) Loan Requirements

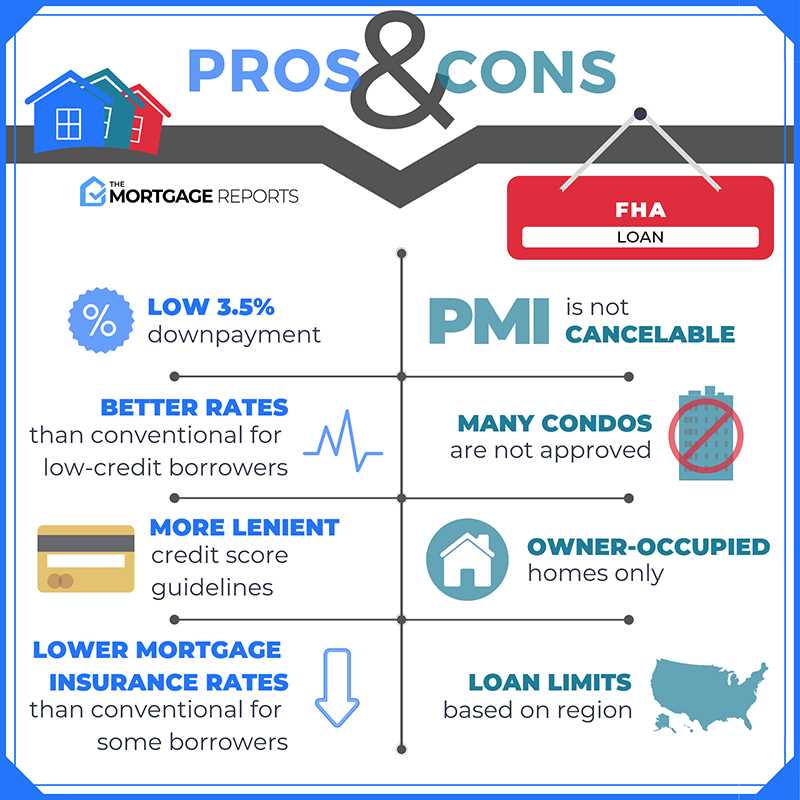

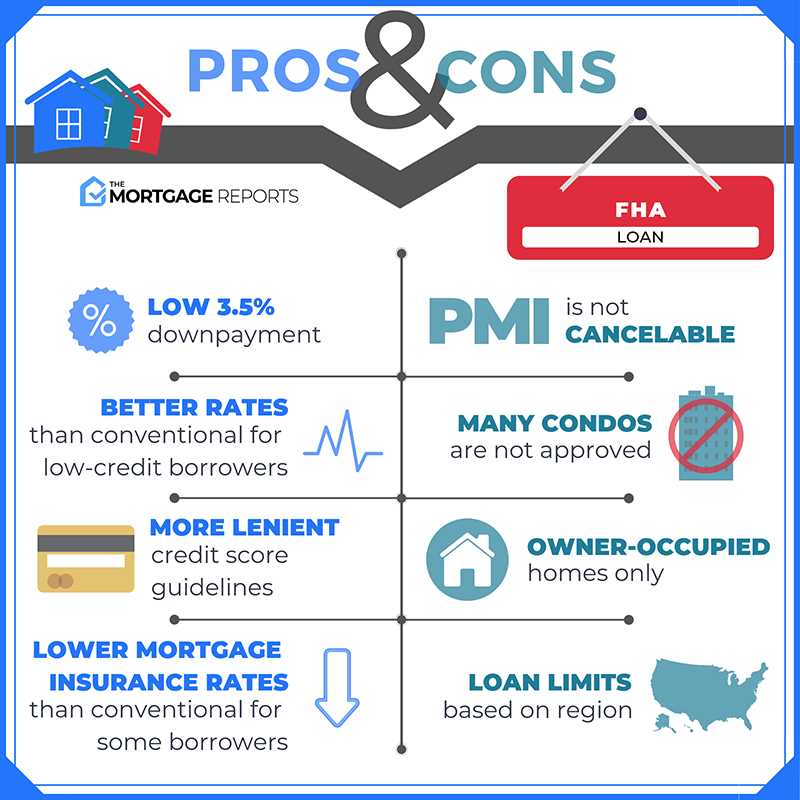

The Federal Housing Administration (FHA) loan program provides mortgage insurance for homebuyers, allowing them to obtain loans with lower down payments and more lenient credit requirements compared to conventional loans. The FHA loan program is administered by the U.S. Department of Housing and Urban Development (HUD) and is designed to help low-to-moderate-income borrowers achieve homeownership.

To qualify for an FHA loan, borrowers must meet certain requirements:

| Requirement | Details |

|---|---|

| Credit Score | Borrowers typically need a minimum credit score of 580 to qualify for the low down payment option (3.5% down). However, borrowers with a credit score between 500 and 579 may still be eligible with a higher down payment (10% down). |

| Debt-to-Income Ratio | The FHA has specific guidelines regarding the ratio of a borrower’s monthly debt payments to their gross monthly income. Generally, the maximum allowable debt-to-income ratio is 43%, although exceptions may be made for borrowers with compensating factors. |

| Down Payment | The minimum down payment required for an FHA loan is 3.5% of the purchase price or appraised value, whichever is less. This is significantly lower than the down payment requirement for conventional loans, which is typically 20%. |

| Property Requirements | The property being purchased with an FHA loan must meet certain standards set by the FHA. These standards include minimum property condition requirements and restrictions on the types of properties that can be financed with an FHA loan. |

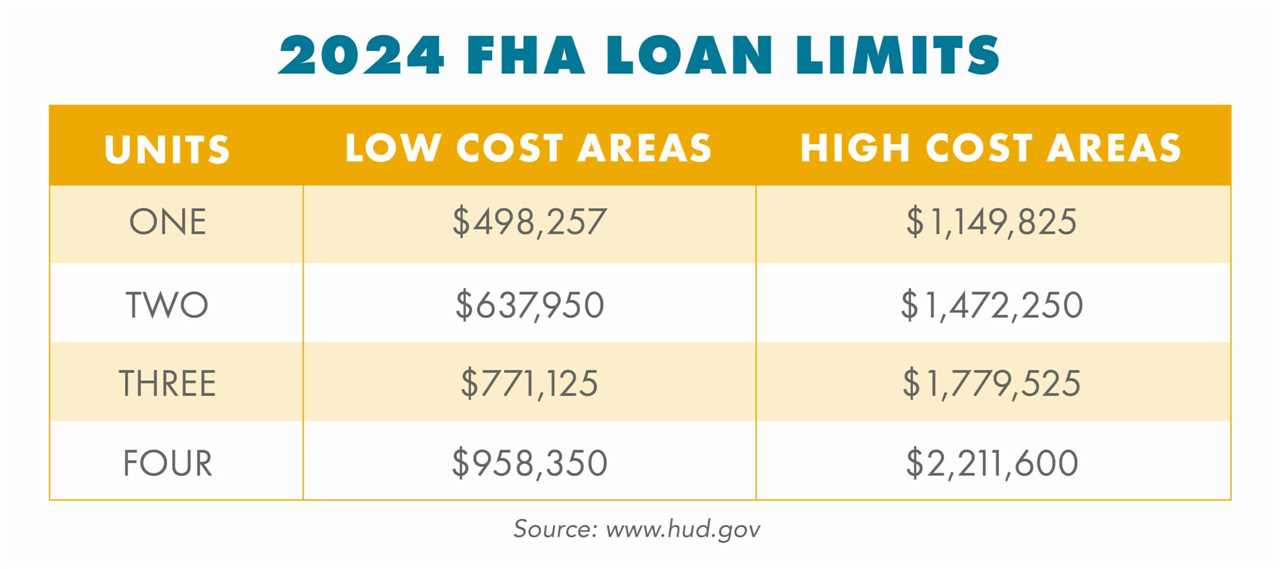

| Loan Limits | The FHA sets limits on the amount of money that can be borrowed using an FHA loan. These limits vary by county and are based on the median home prices in the area. Borrowers should check the FHA loan limits for their specific county before applying. |

Overview of FHA Loan Program

The Federal Housing Administration (FHA) Loan Program is a government-backed mortgage loan program designed to help individuals and families achieve homeownership. The program is administered by the Federal Housing Administration, which is a part of the U.S. Department of Housing and Urban Development (HUD).

The FHA Loan Program offers several benefits to borrowers, including lower down payment requirements and more flexible qualification criteria compared to conventional loans. This makes it an attractive option for first-time homebuyers and individuals with lower credit scores or limited financial resources.

One of the key features of the FHA Loan Program is the low down payment requirement. Borrowers can qualify for an FHA loan with a down payment as low as 3.5% of the purchase price or appraised value of the home, whichever is less. This is significantly lower than the typical 20% down payment required for conventional loans.

In addition to the low down payment requirement, the FHA Loan Program also allows borrowers to use gift funds or grants to cover their down payment and closing costs. This can be a major advantage for individuals who may not have enough savings to cover these expenses on their own.

Furthermore, the FHA Loan Program offers options for borrowers with previous financial hardships, such as bankruptcy or foreclosure. Borrowers who have experienced these events may still be eligible for an FHA loan after a certain waiting period and by meeting specific criteria.

Qualification Limits for FHA Loans

Credit Score Requirements

One of the key factors that lenders consider when determining eligibility for an FHA loan is the borrower’s credit score. While the FHA does not have a specific minimum credit score requirement, most lenders will require a credit score of at least 580 to qualify for the low down payment option. Borrowers with a credit score between 500 and 579 may still be eligible for an FHA loan, but will need to make a larger down payment.

Debt-to-Income Ratio

In addition to credit score, lenders also consider the borrower’s debt-to-income (DTI) ratio when determining eligibility for an FHA loan. The DTI ratio is calculated by dividing the borrower’s monthly debt payments by their gross monthly income.

The FHA sets a maximum DTI ratio of 43% for borrowers applying for an FHA loan. This means that the borrower’s total monthly debt payments, including the mortgage payment, should not exceed 43% of their gross monthly income.

Loan Limits

Another important qualification limit for FHA loans is the loan limit. The FHA sets loan limits based on the county in which the property is located. These limits vary by location and are adjusted annually to reflect changes in the housing market.

The loan limits for FHA loans range from $331,760 to $1,581,750, depending on the county. Borrowers can check the FHA website or contact their lender to find out the loan limits for their specific area.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.