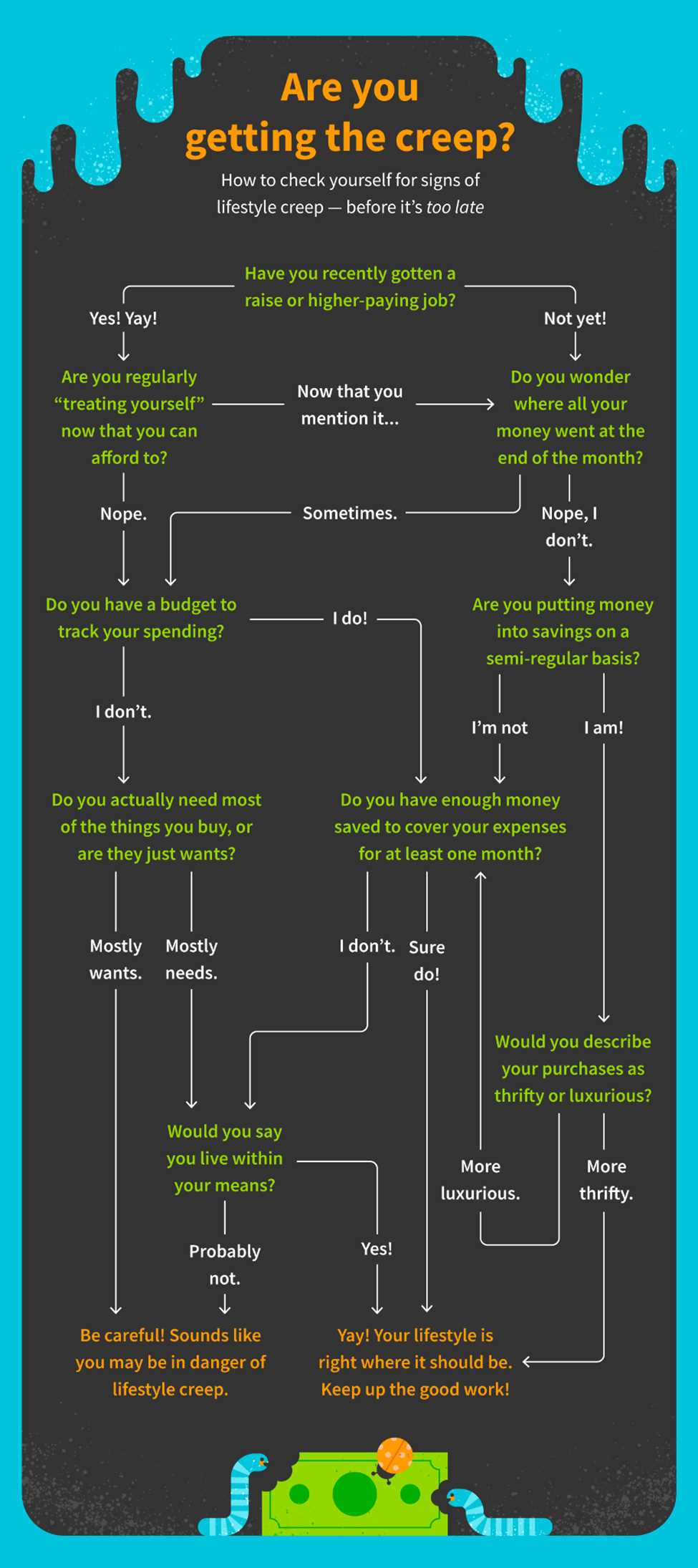

The Definition and Causes of Lifestyle Creep

Lifestyle creep refers to the gradual increase in spending and expenses as an individual’s income increases. It is a phenomenon that occurs when people start earning more money and subsequently upgrade their lifestyle to match their new income level. As a result, they often find themselves living paycheck to paycheck or struggling to save for the future.

There are several causes of lifestyle creep. One of the main causes is the desire to keep up with others and maintain a certain social status. People often feel pressure to spend money on material possessions, luxury goods, and experiences in order to fit in or impress others. This can lead to a never-ending cycle of upgrading and spending more.

Another cause of lifestyle creep is the lack of financial literacy and planning. Many individuals are not aware of the long-term consequences of their spending habits and fail to prioritize saving for the future. They may also lack the knowledge and skills to effectively manage their finances and make informed decisions about their spending.

Additionally, lifestyle creep can be fueled by the availability of easy credit and the temptation to use debt to finance a higher standard of living. With access to credit cards, loans, and other forms of borrowing, it becomes easier for individuals to indulge in immediate gratification and overspend.

Furthermore, lifestyle creep can be influenced by societal and cultural norms. In a consumer-driven society, there is constant pressure to acquire more and have the latest and greatest possessions. Advertisements, social media, and peer influence can all contribute to the desire for a higher standard of living.

The Negative Effects of Lifestyle Creep on Retirement Planning

Lifestyle creep refers to the gradual increase in spending as income increases, often resulting in a higher standard of living. While it may seem harmless at first, lifestyle creep can have significant negative effects on retirement planning.

One of the main negative effects of lifestyle creep is that it can lead to a decrease in savings. As individuals start earning more money, they tend to spend more on discretionary items such as dining out, vacations, and luxury goods. This increased spending leaves less money available for saving and investing for retirement.

Another negative effect of lifestyle creep is the potential for increased debt. As individuals increase their spending, they may rely more on credit cards or loans to fund their lifestyle. This can lead to a cycle of debt, making it even more difficult to save for retirement.

Lifestyle creep can also create a false sense of security. As individuals become accustomed to a higher standard of living, they may assume that their current income will continue indefinitely. However, unexpected events such as job loss or a decrease in income can quickly disrupt this lifestyle. Without adequate savings, individuals may find themselves unprepared for retirement.

Furthermore, lifestyle creep can also impact long-term financial goals. As individuals focus on immediate gratification and increasing their standard of living, they may neglect saving for retirement or other financial milestones. This can result in a lack of financial security in the future.

To combat the negative effects of lifestyle creep on retirement planning, it is important to prioritize saving and investing. Creating a budget and sticking to it can help individuals avoid unnecessary spending and ensure that they are saving enough for retirement. Additionally, regularly reviewing and adjusting financial goals can help individuals stay on track and make necessary adjustments to their spending habits.

Strategies to Avoid or Minimize Lifestyle Creep

Lifestyle creep can have a significant impact on retirement planning, but there are strategies that individuals can employ to avoid or minimize its effects. By being proactive and mindful of their spending habits, individuals can maintain a sustainable lifestyle and ensure they are on track for a comfortable retirement.

1. Set clear financial goals: It is important to establish clear financial goals and prioritize saving for retirement. By setting specific targets, individuals can better track their progress and make informed decisions about their spending habits. This can help prevent lifestyle creep and ensure that retirement savings are not compromised.

2. Create a budget: Developing a budget is essential for managing expenses and avoiding unnecessary spending. By tracking income and expenses, individuals can identify areas where they may be overspending and make adjustments accordingly. A budget can also help individuals allocate a portion of their income towards retirement savings, making it a priority.

3. Differentiate between needs and wants: It is crucial to differentiate between essential needs and discretionary wants. By focusing on fulfilling needs rather than wants, individuals can avoid unnecessary expenses and prevent lifestyle creep. This can involve making conscious decisions about spending and prioritizing long-term financial goals.

5. Automate savings: Automating retirement savings can be an effective way to avoid lifestyle creep. By setting up automatic transfers from a paycheck to a retirement account, individuals can ensure that a portion of their income is consistently allocated towards retirement savings. This removes the temptation to spend the money on discretionary expenses and helps individuals stay on track with their long-term financial goals.

6. Regularly review and adjust: It is important to regularly review and adjust financial plans to account for changes in income, expenses, and goals. By periodically reassessing one’s financial situation, individuals can identify any potential areas of lifestyle creep and make necessary adjustments to stay on track. This can involve increasing retirement savings contributions or cutting back on unnecessary expenses.

7. Seek professional advice: Consulting with a financial advisor can provide valuable guidance and expertise in managing finances and avoiding lifestyle creep. A financial advisor can help individuals develop a personalized financial plan, set realistic goals, and provide strategies for minimizing lifestyle creep. They can also provide ongoing support and accountability to ensure individuals stay on track with their retirement planning.

By implementing these strategies, individuals can avoid or minimize lifestyle creep and ensure they are on the path to a secure retirement. It requires discipline, awareness, and a commitment to long-term financial planning, but the benefits of maintaining a sustainable lifestyle and achieving financial security in retirement are well worth the effort.

The Importance of Long-Term Financial Planning in Combating Lifestyle Creep

The Impact on Retirement Planning

Lifestyle creep can have a detrimental effect on retirement planning. By increasing spending without considering long-term financial goals, individuals may find themselves unable to save enough for retirement. They may become accustomed to a higher standard of living and find it challenging to scale back their expenses when they reach retirement age. This can lead to financial stress and a reduced quality of life during retirement.

Additionally, lifestyle creep can also lead to a reliance on debt to maintain the desired standard of living. Individuals may resort to credit cards or loans to finance their increased spending, which can further hinder their ability to save for retirement.

Strategies to Avoid or Minimize Lifestyle Creep

To combat lifestyle creep and ensure a secure financial future, it is essential to implement strategies that help avoid or minimize its impact. Here are some strategies to consider:

- Create a budget: Establish a budget that takes into account both short-term and long-term financial goals. Allocate a portion of your income towards savings and investments to ensure you are actively working towards your retirement goals.

- Automate savings: Set up automatic transfers to a retirement account or investment vehicle. By automating your savings, you are less likely to succumb to the temptation of increased spending.

- Regularly review expenses: Periodically review your expenses to identify areas where you can cut back. Consider whether certain purchases align with your long-term financial goals and make adjustments accordingly.

- Avoid lifestyle inflation: Resist the urge to increase your spending every time your income rises. Instead, focus on maintaining a consistent standard of living and prioritize saving for the future.

- Seek professional advice: Consider consulting with a financial advisor who can help you develop a comprehensive retirement plan and provide guidance on managing lifestyle creep.

Conclusion

While lifestyle creep may be tempting, it is crucial to prioritize long-term financial planning to combat its negative effects. By creating a budget, automating savings, reviewing expenses, avoiding lifestyle inflation, and seeking professional advice, individuals can ensure a secure financial future and enjoy a comfortable retirement.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.