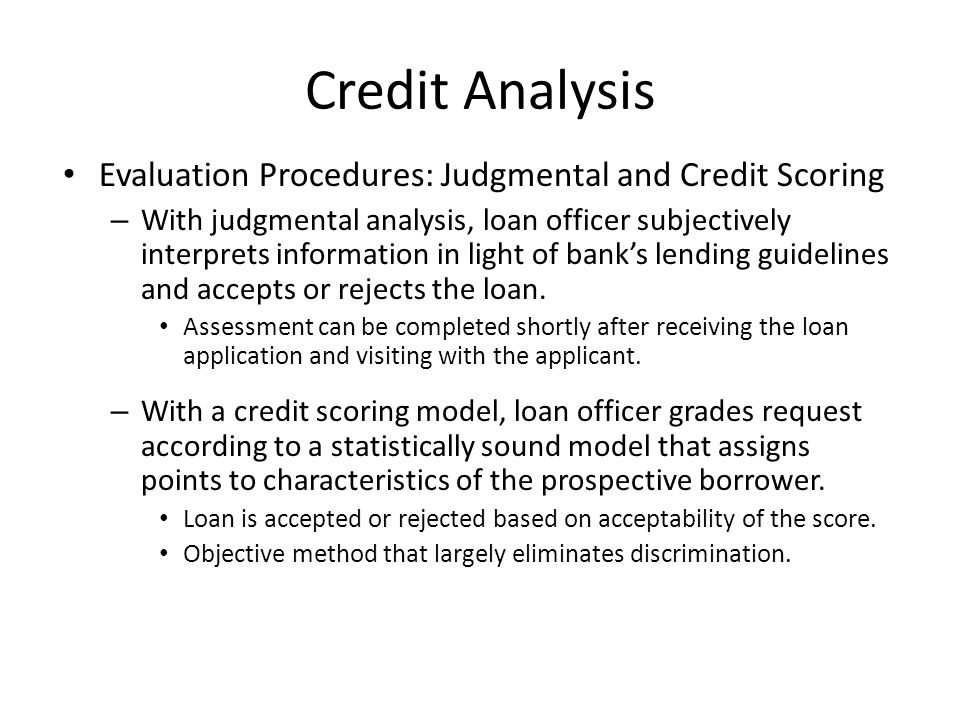

Why is Credit Analysis Important?

Introducing Judgmental Credit Analysis

Our comprehensive guide, “Judgmental Credit Analysis: A Comprehensive Guide to Assessing Borrower’s Creditworthiness,” is designed to equip banking professionals with the knowledge and tools they need to make informed lending decisions.

What You’ll Learn:

- The fundamentals of credit analysis

- How to evaluate a borrower’s financial statements

- Assessing the borrower’s repayment capacity

- Identifying potential credit risks

- Using qualitative factors in credit analysis

Why Choose Our Guide?

- Practical: We provide real-life examples and case studies to help you apply the concepts in a practical setting.

- Expert Insights: Learn from industry experts who have years of experience in credit analysis.

- Up-to-Date: Our guide is regularly updated to reflect the latest trends and best practices in credit analysis.

Don’t leave your lending decisions to chance. Invest in your knowledge and get our guide, “Judgmental Credit Analysis: A Comprehensive Guide to Assessing Borrower’s Creditworthiness,” today!

1. Minimizing Default Risk

One of the primary reasons for assessing creditworthiness is to minimize the risk of default. Default occurs when a borrower fails to repay their loan or meet their financial obligations. By evaluating the creditworthiness of borrowers, banks can identify individuals or businesses with a higher likelihood of defaulting and adjust their lending terms accordingly. This helps protect the bank’s assets and ensures a more stable lending portfolio.

2. Determining Interest Rates

Creditworthiness assessment also plays a significant role in determining the interest rates offered to borrowers. Individuals or businesses with a higher creditworthiness are considered less risky and may qualify for lower interest rates. On the other hand, borrowers with a lower creditworthiness may be charged higher interest rates to compensate for the increased risk. By accurately assessing creditworthiness, banks can offer competitive interest rates that align with the risk profile of the borrower.

Additionally, creditworthiness assessment helps banks differentiate between borrowers with varying levels of creditworthiness. This allows them to tailor loan terms, such as repayment periods and loan amounts, to meet the specific needs and abilities of each borrower. This personalized approach enhances customer satisfaction and increases the likelihood of successful loan repayment.

3. Improving Loan Approval Process

By assessing creditworthiness, banks can streamline the loan approval process. They can quickly identify borrowers who meet the necessary credit requirements and have a higher probability of repaying their loans. This reduces the time and resources spent on evaluating loan applications that are likely to be rejected. A more efficient loan approval process benefits both the bank and the borrower, ensuring a faster turnaround time and a smoother borrowing experience.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.