Benefits of Health Savings Accounts (HSAs)

Health Savings Accounts (HSAs) offer a range of benefits for individuals and families. Here are some key advantages of having an HSA:

1. Tax Advantages

Contributions made to an HSA are tax-deductible, meaning that you can reduce your taxable income by the amount you contribute. This can result in significant tax savings, especially for those in higher tax brackets.

Additionally, any interest or investment earnings on the funds in your HSA are tax-free. This allows your savings to grow over time without being subject to taxes.

2. Flexibility

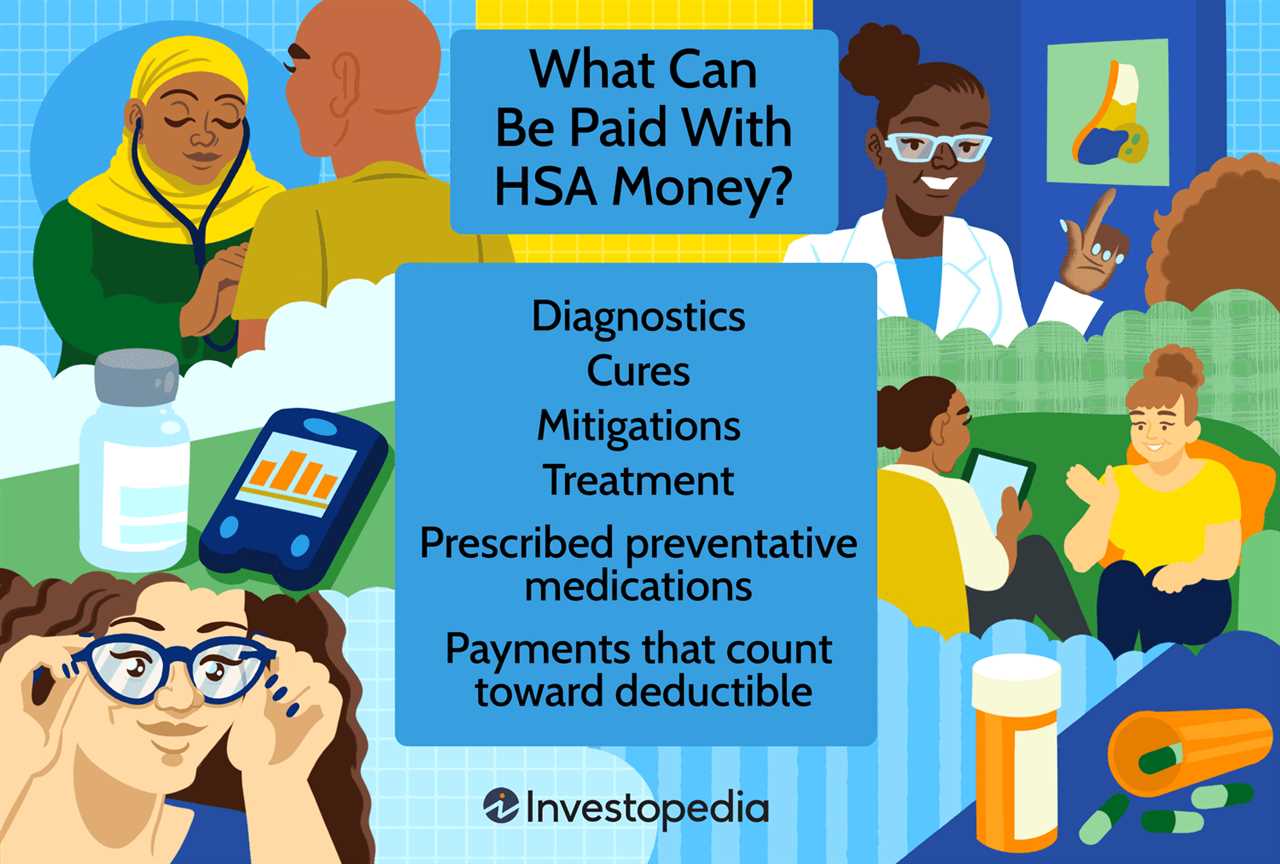

HSAs offer flexibility in how you can use the funds. While the primary purpose of an HSA is to cover qualified medical expenses, you can also use the funds for other purposes. After the age of 65, you can withdraw funds for any reason without incurring a penalty, although you will still need to pay income tax on the amount withdrawn if it is not used for qualified medical expenses.

Furthermore, HSAs are portable, meaning that you can take your account with you if you change jobs or retire. This allows you to continue saving and using the funds for medical expenses even if your employment situation changes.

3. Savings for the Future

One of the main advantages of an HSA is the ability to save for future medical expenses. Unlike a Flexible Spending Account (FSA), the funds in an HSA roll over from year to year, so you don’t have to worry about losing any unused funds at the end of the year.

This makes an HSA a great tool for building a nest egg for healthcare costs in retirement. By contributing regularly to your HSA and allowing the funds to grow over time, you can ensure that you have a dedicated source of funds for medical expenses later in life.

Contribution Limits and Rules

1. Annual Contribution Limits

2. Catch-Up Contributions

Individuals who are 55 years or older can make additional catch-up contributions to their HSAs. For 2021, the catch-up contribution limit is $1,000. This allows older individuals to save more for their healthcare expenses.

3. Contribution Deadlines

4. Employer Contributions

Employers can also contribute to their employees’ HSAs. These contributions are tax-deductible for the employer and do not count towards the employee’s annual contribution limit. This can be a valuable benefit for employees and can help boost their HSA savings.

5. Excess Contributions

If you accidentally contribute more than the annual limit to your HSA, you have until the tax filing deadline to remove the excess amount. Otherwise, the excess contributions will be subject to a 6% excise tax.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.