Explaining Efficiency in Economics

In economics, efficiency refers to the ability to produce the maximum output with the given resources. It is an important concept that helps us understand how well an economy is utilizing its resources to meet the needs and wants of its population.

Types of Efficiency

There are two main types of efficiency in economics:

- Allocative Efficiency: This type of efficiency occurs when resources are allocated in such a way that the production of one good or service cannot be increased without decreasing the production of another good or service. In other words, it is the optimal allocation of resources to maximize the overall welfare of the society.

- Productive Efficiency: Productive efficiency occurs when an economy is producing goods and services at the lowest possible cost. It means that resources are being used in the most efficient way to produce the maximum output.

Measuring Efficiency

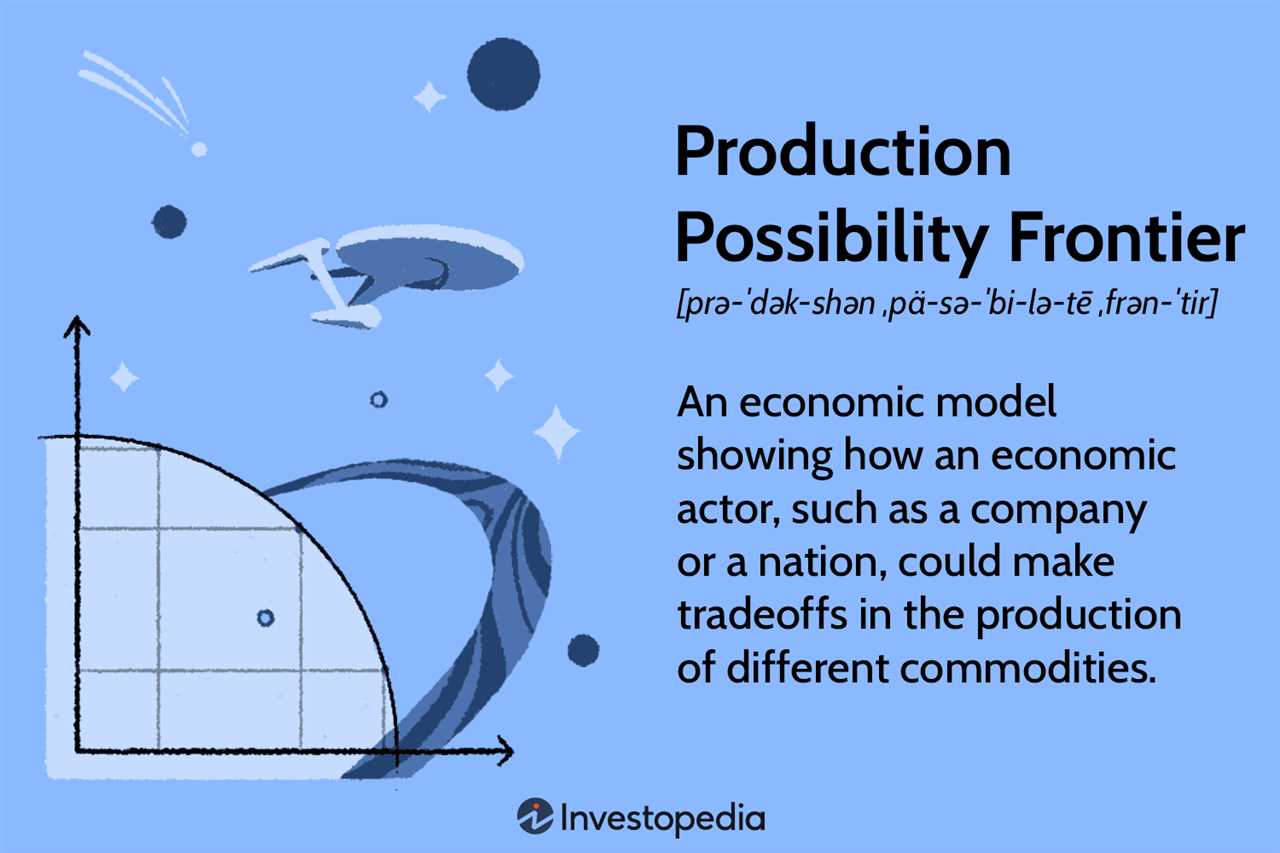

Efficiency can be measured using various indicators and tools. One commonly used tool is the Production Possibility Frontier (PPF) curve graph. The PPF curve shows the maximum possible combinations of two goods that an economy can produce given its resources and technology.

The PPF curve graph visually represents the trade-offs between producing different goods. It illustrates the concept of opportunity cost, which is the cost of giving up one good in order to produce more of another good. The slope of the PPF curve represents the opportunity cost of producing one good in terms of the other.

Importance of Efficiency

Efficiency is crucial for the overall economic growth and development of a country. When an economy operates at its maximum efficiency, it can produce more goods and services, leading to higher living standards and improved quality of life for its citizens.

Efficiency also plays a role in resource conservation and sustainability. By using resources efficiently, an economy can minimize waste and reduce its environmental impact. This is particularly important in the face of limited resources and growing concerns about climate change and environmental degradation.

Conclusion

Efficiency is a fundamental concept in economics that helps us understand how well an economy is utilizing its resources. Allocative efficiency ensures the optimal allocation of resources, while productive efficiency ensures the lowest possible cost of production. Measuring efficiency using tools like the PPF curve graph and formulas like the efficiency ratio allows economists to assess the performance of an economy and identify areas for improvement. By striving for efficiency, economies can achieve higher levels of output, improve living standards, and promote sustainable development.

Emily Bibb simplifies finance through bestselling books and articles, bridging complex concepts for everyday understanding. Engaging audiences via social media, she shares insights for financial success. Active in seminars and philanthropy, Bibb aims to create a more financially informed society, driven by her passion for empowering others.